Australia's Climate Disclosure Mandate: What AASB S2 Means for Your Business Before July 2026

Australia's largest companies have been producing mandatory climate disclosure reports since January 2025. The first of those reports, for Group 1 entities with a 30 June financial year-end, landed with ASIC in October 2025. ASIC is reviewing them.

For Group 2 companies, the clock is now running. Financial years beginning on orafter 1 July 2026 trigger mandatory AASB S2 compliance, which means companieswith 30 June year-ends have roughly three months to confirm they are in scope,stand up their governance disclosures, map their Scope 1 and 2 emissions data,and decide on their reporting infrastructure. What goes wrong in that windowtends to follow companies for years because the same auditor who signs off onyour financial statements will also sign off on your sustainability report.

Thisguide covers the full AASB S2 climate disclosure mandate: who it catches, whatit requires, what the assurance and liability framework looks like, and what aGroup 2 company should be doing right now.

What Is AASB S2 and Where Did It Come From?

AASB S2 (Australian Sustainability Reporting Standard S2: Climate-related Disclosures) is Australia's mandatory standard for climate-related financial reporting, embedded in the Corporations Act 2001. It requires in-scope entities to disclose climate-related risks and opportunities that could reasonably affect their cash flows, access to finance, or cost of capital over the short, medium, and long term.

Thestandard is substantively based on IFRS S2, issued by the International Sustainability Standards Board(ISSB) in June 2023. Australia adopted it via the Australian Accounting Standards Board (AASB), with Australian-specificmodifications covering the liability framework, assurance pathway, andalignment with the National Greenhouse and Energy Reporting Act 2007 (NGER Act). The legal mechanism that made it mandatory was the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024, whichpassed Parliament in September 2024.

AASBS1, the general sustainability reporting standard, is voluntary. AASB S2 is mandatory. If you are in scope, you are required to produce a climate-specific sustainability report alongside your annual financial report, lodged with ASI Con the same schedule as your financial statements.

ASIC Chair Joe Longo described the regime at the Deakin Law School International Sustainability Reporting Forum as "the biggest changes to financialreporting and disclosure standards in a generation." More than 6,000Australian entities will be required to report under the new requirementsacross the three phases.

TheDecember 2025 AASB amendments aligned the standard with ISSB's targetedclarifications to IFRS S2, introducing relief measures for certain Scope 3Category 15 emissions disclosures and adjustments to global warming potentialvalues. These amendments are effective for financial years beginning on orafter 1 January 2027, with early adoption permitted.

Source: ASIC Chair Joe Longo, Deakin Law School International Sustainability Reporting Forum keynote, April 2024; AASB S2 December 2025 amendments.

Who Must Report?

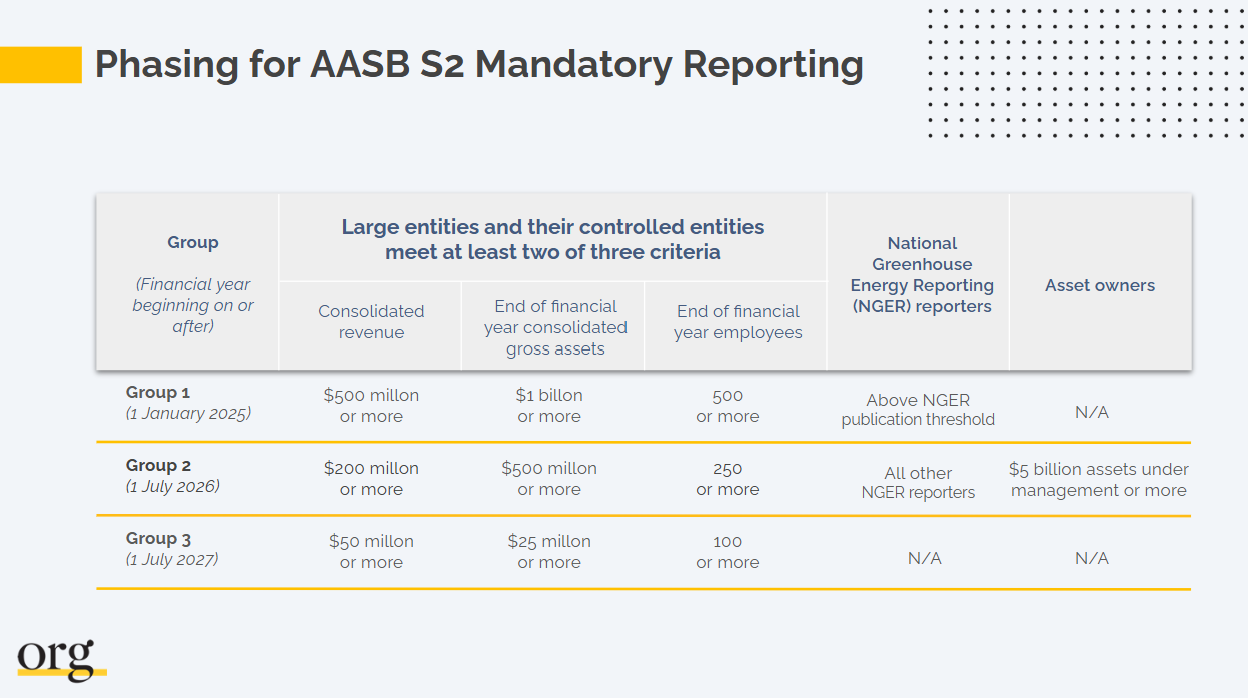

Does my company need to report under AASB S2? Your company must report if it prepares annualfinancial reports under Chapter 2M of the Corporations Act 2001 and meets twoof the three size thresholds for its group. NGER Act reporters above a certainemissions threshold are also captured regardless of size. Group 1 reportingbegan January 2025. Group 2 begins July 2026. Group 3 begins July 2027.

Source: AASB S2 Climate-related Disclosures (October 2024,amended December 2025); PwC Australia Sustainability Reporting Guide.

The two-of-three rule.

An entity meets the threshold if it satisfies two of the three criteria revenue, assets, and employee count. A company with 300 employees and A $200M in revenuebut only A$400M in assets still qualifies for Group 2 because it meets the revenue and employee criteria. Part-time employees count as a fractional full-time equivalent under ASIC's guidance.

The NGER catch-all.

Entitiesthat report under the National Greenhouse and Energy Reporting Act and haveemitted 50 kilotons or more of carbon dioxide equivalent are captured underGroup 1 thresholds, regardless of revenue or asset size. This pulls insignificant emitters who might otherwise believe they sit below the financialthreshold.

Super funds and asset owners managingA$5 billion or more in assets must report from Group 2 onwards. ASIC's RG 280clarified that the threshold is based on the value of assets.

The Group 3 materiality exemption is not a blanket opt-out.

Companies must conduct a formal, documentedmateriality assessment and make a director declaration explaining theirconclusion. Without that documentation, the exemption claim will not withstandaudit scrutiny or regulatory challenge. In practice, most Group 3 entities willneed the same data infrastructure as Groups 1 and 2 just to prove they qualifyfor the exemption.

Entitiesoutside mandatory scope but inside voluntary pressure: institutional investorrequirements, lender covenants, and supply chain due diligence increasinglypull smaller companies into de facto climate disclosure regardless of mandatorystatus. If your company is a tier-two supplier to an ASX 200 company nowreporting under AASB S2, expect disclosure requests.

What Does AASB S2 Actually Require You to Disclose?

AASBS2 is structured around four disclosure pillars the same architecture as IFRS S2 and the former TCFD (Task Force on Climate-related Financial Disclosures) recommendations. For readers new to TCFD: it was the voluntary global climate disclosure framework that AASB S2 has effectively replaced in Australia with amendatory, auditable version.

Pillar 1: Governance

Boards must disclose how they oversee climate-related risks and opportunities. This isnot a generic statement about sustainability commitments. AASB S2 asks forspecifics: which board committee has formal climate oversight, how often theboard receives climate risk updates, and what expertise or external supportinforms those reviews.

Formany Australian companies, particularly mid-market companies enteringcompliance at Group 2, this requires formal board resolutions and updatedcommittee charters before the first sustainability report can be drafted. Thegovernance section is subject to limited assurance from Year 1, meaning yourauditor will scrutinize the accuracy of these disclosures from the firstreport.

Pillar 2: Strategy

This is the section most companies underestimate. AASB S2 requires entities todescribe the climate-related risks and opportunities that could reasonably beexpected to affect their business, and to assess the financial impact of thoserisks under at least two climate scenarios.

Australia'smandatory scenario requirements are specific. The AASB requires entities to useat least two scenarios:

• A 1.5°C scenario — aligned withAustralia's Climate Change Act 2022

• A 2.5°C orhigher scenario — representing ahigh physical risk pathway

ForGroup 2 companies with limited internal ESG capability, conducting crediblescenario analysis before July 2026 is one of the most resource-intensiverequirements in the standard. Companies that have not started this work arebehind.

TheStrategy pillar also covers transition plans on how the company intends tomanage climate-related risks over time, including any capital allocationdecisions, operational changes, or technology investments tied to those plans.

Pillar 3: Risk Management

Entitiesmust describe how they identify, assess, and manage climate-related risks, andhow those processes integrate with overall enterprise risk management. Thedistinction regulators are watching for: is climate risk treated as astandalone ESG exercise, or is it embedded in the same frameworks used forfinancial and operational risk? Reports where climate risk sits in a separatedocument from the board's main risk register will attract scrutiny.

Pillar 4: Metrics and Targets

Thisis where the data infrastructure requirement becomes concrete.

Year 1 (first reporting period):

Scope1 and Scope 2 greenhouse gas (GHG) emissions are mandatory. Scope 1 coversdirect emissions from sources the company controls like fuel combustion,industrial processes, company vehicles. Scope 2 covers indirect emissions frompurchased electricity, heat, or steam. Three-year transitional relief appliesto market-based Scope 2 emissions, meaning companies can use location-based figuresin Year 1.

Year 2 onwards:

Scope 3 emissions become mandatory. Scope 3 covers all indirect emissions across the value chain like purchased goods and services, business travel, employee commuting, product use, and end-of-life treatment. For most Australian companies, Scope 3 represents the largest and most complex portion of their total carbon footprint, and it is the one area where data gaps are most likely to cause audit problems.

December2025 development: The AASB aligned AASB S2 with ISSB's targeted amendments introducing specific relief for Scope 3 Category 15 financed emissions like material for Australian banks, asset managers, and insurers using PCAF (Partnership for Carbon Accounting Financials) methodology. PCAF is the industry-standard method for measuring emissions associated with loans and investments. Relief applies from financial years beginning on or after 1January 2027, with early adoption permitted.

Companiesmust also disclose climate-related targets, not just aspirational net-zerocommitments, but specific, measurable targets with defined base years andmetrics. Vague language about "working toward" emissions reductionsis not compliant.

The Assurance Timeline: What Gets Audited and When

Theassurance requirements are where AASB S2 diverges most sharply from voluntaryframeworks. This is not a self-certification exercise. Your sustainabilityreport will be audited and the auditor must be the same firm that audits yourfinancial statements.

TheAustralian Auditing and Assurance Standards Board (AUASB) adopted ASSA 5000(General Requirements for Sustainability Assurance Engagements) and ASSA 5010(Timeline for Audits and Reviews of Sustainability Reports) in January 2025.These are the standards your external auditor will apply.

Year 1, Limited assurance on:

• Governancedisclosures (Paragraph 6 of AASB S2)

• Scope 1 andScope 2 GHG emissions

Allother disclosures, strategy, risk management, targets, scenario analysis, arenot subject to assurance in Year 1, though they must still be disclosedaccurately. The modified directors' declaration (applicable for financial yearsbetween 1 January 2025 and 30 December 2027) requires directors to declare thatthe entity has taken "reasonable steps" to ensure the sustainabilityreport's substantive provisions comply with the Act.

Years 2 and 3, Limited assurance expands

Limitedassurance covers all components of the sustainability report, including Scope 3emissions, scenario analysis disclosures, and transition plans.

From 1 July 2030, Reasonable assurance

Reasonableassurance applies across all disclosures, the same standard applied to auditedfinancial statements. At this point, the bar for data quality, methodologydocumentation, and internal controls over climate data is equivalent to whatcompanies currently maintain for their accounts.

Companiestreating Year 1 as a soft launch are building habits and systems that will needto withstand reasonable assurance within four years. Auditors who beginreviewing sustainability reports in 2026 will carry institutional memory of howa company's data infrastructure was set up and the quality of thatinfrastructure will become a recurring audit risk if it is not built correctlyfrom the start.

Threethings auditors are already asking Group 1 companies and that Group 2 companiesshould be answering before they file:

1. Where doesyour Scope 1 and Scope 2 data come from, and can you produce an audit trail tosource data?

2. How does yourclimate risk identification process connect to your board risk register?

3. What internalcontrols exist over the emissions calculation methodology?

5. What Directors Face: The LiabilityFramework

What are the penalties for non-compliance with AASB S2?

Non-compliance with AASB S2 can result in civil penalties for directors ranging from A$93,900to A$751,200 per offence under the Corporations Act 2001, enforced by ASIC. Additional offences include failure to keep sustainability records and failureto comply with ASIC directions. ASIC can also direct companies to correct oramend reports without commencing formal proceedings.

Source: Corrs Chambers Westgarth; Corporations Act 2001.

ASIC's new direction powers.

Underthe regime, ASIC has the authority to direct a company to correct, complete, oramend a statement in a sustainability report if it believes the statement isincorrect, incomplete, or misleading without having to issue infringementnotices or commence enforcement proceedings. This is a lower threshold thantraditional enforcement action.

The modified liability period (2025–2027) is not immunity.

Forfinancial years beginning between 1 January 2025 and 31 December 2027, certainforward-looking statements like Scope 3 emissions, scenario analysis,transition plans, and climate-related forward-looking statements are shieldedfrom private civil action. Only ASIC can bring action on these protectedstatements during the transition window. ASIC's enforcement ability is notsuspended.

Greenwashingprecedent is already established. In 2025, the Federal Court ordered a A$10.5million penalty against a superfund for investing in coal mining whilerepresenting to members that such investments were eliminated under its ESG criteria. ASIC commenced a further greenwashing proceeding in October 2025, thefirst to target a responsible entity using Corporations Act duties as a causeof action.

ASIC has stated that greenwashing will not be an explicit enforcement priority in2026. That is not a signal to relax. It reflects ASIC's stated intention totake a pragmatic approach to the first year of mandatory reporting, not a suspension of its enforcement mandate. ASIC's 2025–2026 Corporate Plan explicitly lists climate reporting as a strategic priority alongside financialreporting, auditor conduct, and director accountability.

Source: Ashurst, Climate Litigation in Australia: Key Developments in 2025 and What's Ahead for 2026, February 2026.

What Group 2 Companies Need to Do Before July 2026

Threemonths. That is the approximate window between today and the start of the First Group 2 reporting period for companies with a 30 June financial year. Forcalendar year-end companies, reporting begins 1 January 2027 which soundsfurther away but is not, given how long it takes to build a data collectioninfrastructure from scratch.

Thesix steps that cannot be deferred:

Step 1: Confirm scope. Run the two-of-three threshold test against your most recent audited financials. Check NGER obligations independently some companies are NGER reporters without realizing their emissions threshold pulls them into AASB S2 scope earlier than expected. If you are on the margin, get a legal opinion before assuming you are out.

Step 2: Conduct a climate materiality assessment. Before you can write any section of thesustainability report, you need to know which climate-related risks andopportunities are material to your specific business. A real estate companywith significant coastal assets faces different material physical risks than alogistics operator with a diesel fleet. Materiality assessment is also thelegal basis for a Group 3 exemption and it requires documented methodology, notjust a board-level judgment call.

Step 3: Map your emissions data gaps. Scope 1 and Scope 2 data must be disclosed in yourfirst report. Many companies that have been tracking emissions informally willfind that their existing data is not audit-ready. Emissions calculations need adocumented methodology, source data traceability, and a record of assumptionsused. Start the gap assessment now rather than discovering the problem in theweek before filing.

Step 4: Engage your auditor early. The firm auditing your financial statements will also audit yoursustainability report. They need lead time to understand your business, yourclimate risk profile, and your data systems. Auditors are already building AASBS2 review capacity, and the firms with the most experience are allocating thatcapacity to clients who engaged them early. Waiting until Q4 2026 to begin theaudit conversation is a risk management failure.

Step 5: Stand up governance documentation. The Governance pillar, board committee mandates,climate risk review frequency, director expertise or external advisoryarrangements, is subject to limited assurance from Year 1. Board resolutions,committee charters, and board paper templates need to be in place anddocumented before the first sustainability report is drafted. A retrospectivegovernance narrative written in the reporting period is not the same ascontemporaneous evidence of board oversight.

Step 6: Decide on reporting infrastructure. The options are: build internally usingspreadsheets and manual aggregation; engage a Big Four or specialist advisoryfirm for a managed service; or implement a purpose-built ESG platform thatintegrates emissions data collection, calculation, scenario analysis, andreport generation into a single auditable system. For a Group 2 companyproducing its first audited sustainability report with Scope 3 obligationskicking in Year 2, a spreadsheet-based system creates audit risk that compoundseach year.

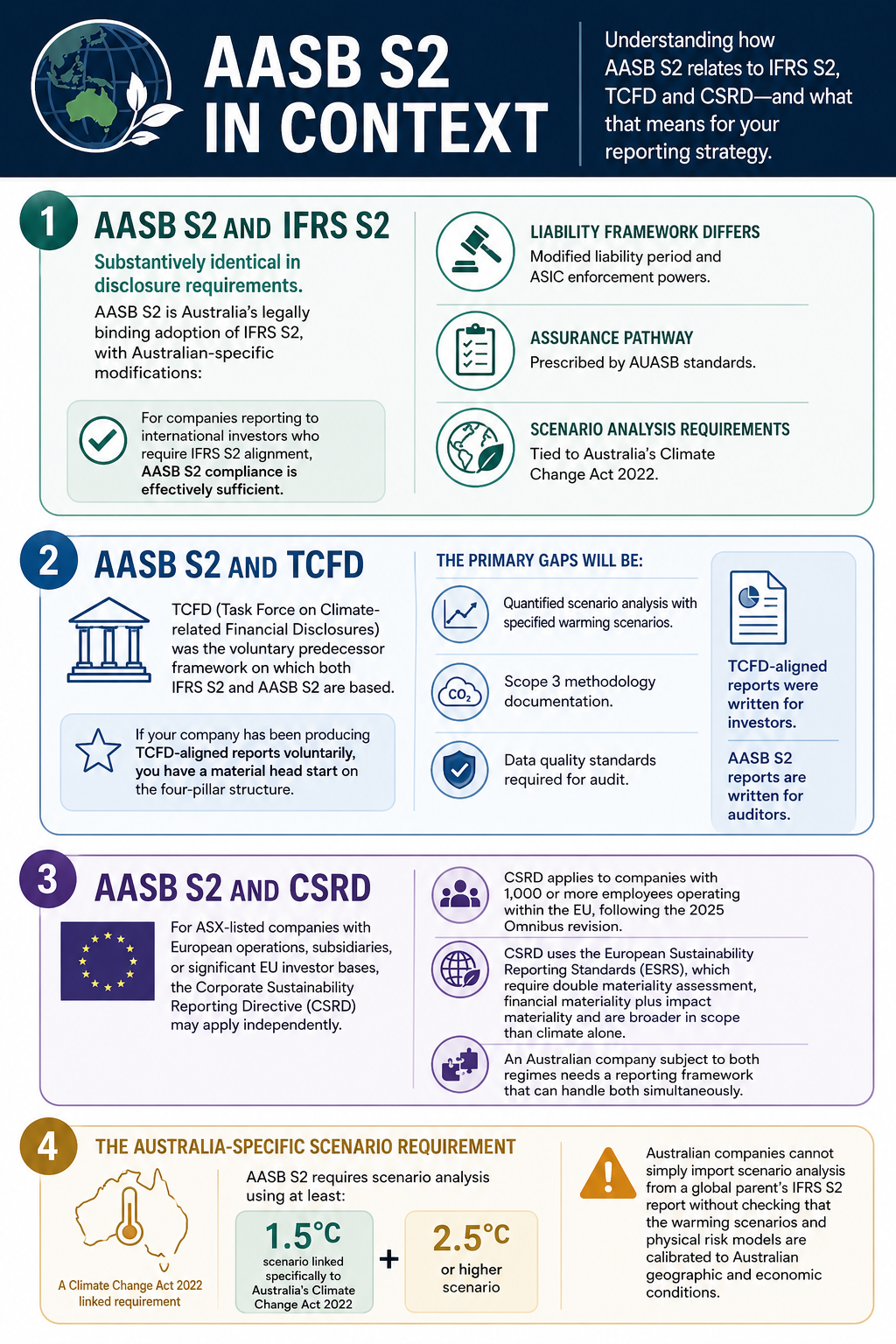

How AASB S2 Compares to Global Standards

For ASX-listed companies with international investors, global parent companies, or operations in Europe, the relationship between AASB S2 and other mandatory frameworks matters.

AASB S2 and IFRS S2. Substantively identical in disclosure requirements. AASB S2 is Australia's legally binding adoption of IFRS S2, with Australian-specific modifications: the liability framework differs (modified liability period, ASIC enforcement powers), the assurance pathway is prescribed by AUASB standards, and the scenario analysis requirements are tied to Australia's Climate Change Act 2022. For companies reporting to international investors who require IFRS S2 alignment, AASB S2 compliance is effectively sufficient.

AASB S2 and TCFD. TCFD (Task Force on Climate-related Financial Disclosures) was the voluntary predecessor framework on which both IFRS S2 and AASB S2 are based. If your company has been producing TCFD-aligned reports voluntarily, you have a material head start on the four-pillar structure. The primary gaps will be: quantified scenario analysis with specified warming scenarios, Scope 3 methodology documentation, and the data quality standards required for audit. TCFD-aligned reports were written for investors. AASB S2 reports are written for auditors.

AASB S2 and CSRD. For ASX-listed companies with European operations, subsidiaries, or significant EU investor bases, the Corporate Sustainability Reporting Directive (CSRD) may apply independently. CSRD applies to companies with 1,000 or more employees operating within the EU, following the 2025 Omnibus revision. CSRD uses the European Sustainability Reporting Standards (ESRS), which require double materiality assessment, financial materiality plus impact materiality and are broader in scope than climate alone. An Australian company subject to both regimes needs a reporting framework that can handle both simultaneously.

The Australia-specific scenario requirement. AASB S2 requires scenario analysis using at least a 1.5°C scenario linked specifically to Australia's Climate Change Act 2022, and a 2.5°C or higher scenario. Australian companies cannot simply import scenario analysis from a global parent's IFRS S2 report without checking that the warming scenarios and physical risk models are calibrated to Australian geographic and economic conditions.

Frequently Asked Questions (FAQs)

What is AASB S2 and is it mandatory?

AASB S2 is Australia's mandatory climate disclosure standard, embedded in the Corporations Act 2001. It applies to in-scope entities meeting two of three size thresholds across revenue, assets, and employee count. AASB S1 (general sustainability reporting) remains voluntary as of April 2026.

When does AASB S2 apply to Group 2 companies?

Group 2 companies must report for financial years beginning on or after 1 July 2026. For companies with a 30 June year-end, the first AASB S2 sustainability report covers the year ending 30 June 2027, typically lodged with ASIC by October 2027.

Does AASB S2 require Scope 3 emissions reporting?

Not in Year 1. Scope 1 and Scope 2 emissions are required from the first reporting period. Scope 3 becomes mandatory from Year 2. The December 2025 AASB amendments introduced targeted relief for Scope 3 Category 15 financed emissions, effective from financial years beginning on or after 1 January 2027.

What happens if we don't comply with AASB S2?

ASIC can direct companies to correct or amend sustainability reports, issue infringement notices, and commence civil penalty proceedings. Director penalties range from A$93,900 to A$751,200 per offence. Additional offences apply for failure to maintain sustainability records. The Federal Court ordered a A$10.5M penalty against a superfund for greenwashing in 2025.

Is AASB S2 the same as IFRS S2?

Substantively, yes. AASB S2 is Australia's adoption of IFRS S2. Disclosure requirements are nearly identical. Key differences are Australian-specific: the liability framework, the assurance pathway governed by AUASB standards, and the scenario analysis requirement tied to Australia's Climate Change Act 2022.

Three Months Is Not Much Time

Group 1 companies are already filing. ASIC is already reviewing. The enforcement,audit, and liability infrastructure is operational.

ForGroup 2 companies, the six preparation steps above are not a checklist to startin June. Climate materiality assessments take weeks. Auditor engagementrequires lead time. Emissions data gaps, once discovered, can take months toclose if source systems are not integrated and calculation methodologies arenot documented.

Thecompanies that will find July 2026 manageable are the ones that started thiswork in early 2026 with a clear scope determination, a structured datacollection process, and reporting infrastructure that produces an audit trail,not a spreadsheet.

Ready to assess your AASB S2 readiness? Spectreco's team works with Group 2 and Group 3companies across financial services, real estate, and data centres to close thegap between current emissions data infrastructure and what AASB S2 actuallyrequires. Book a 30-minute AASB S2 readiness assessment at spectreco.com.

More From Our Blog

Your ESG Journey?