Financed Emissions: What Pakistani Banks Must Do Under SECP IFRS S2 | Spectreco

Financed Emissions 101: What Pakistani Banks Need to Know Before SECP's IFRS S2 Deadline

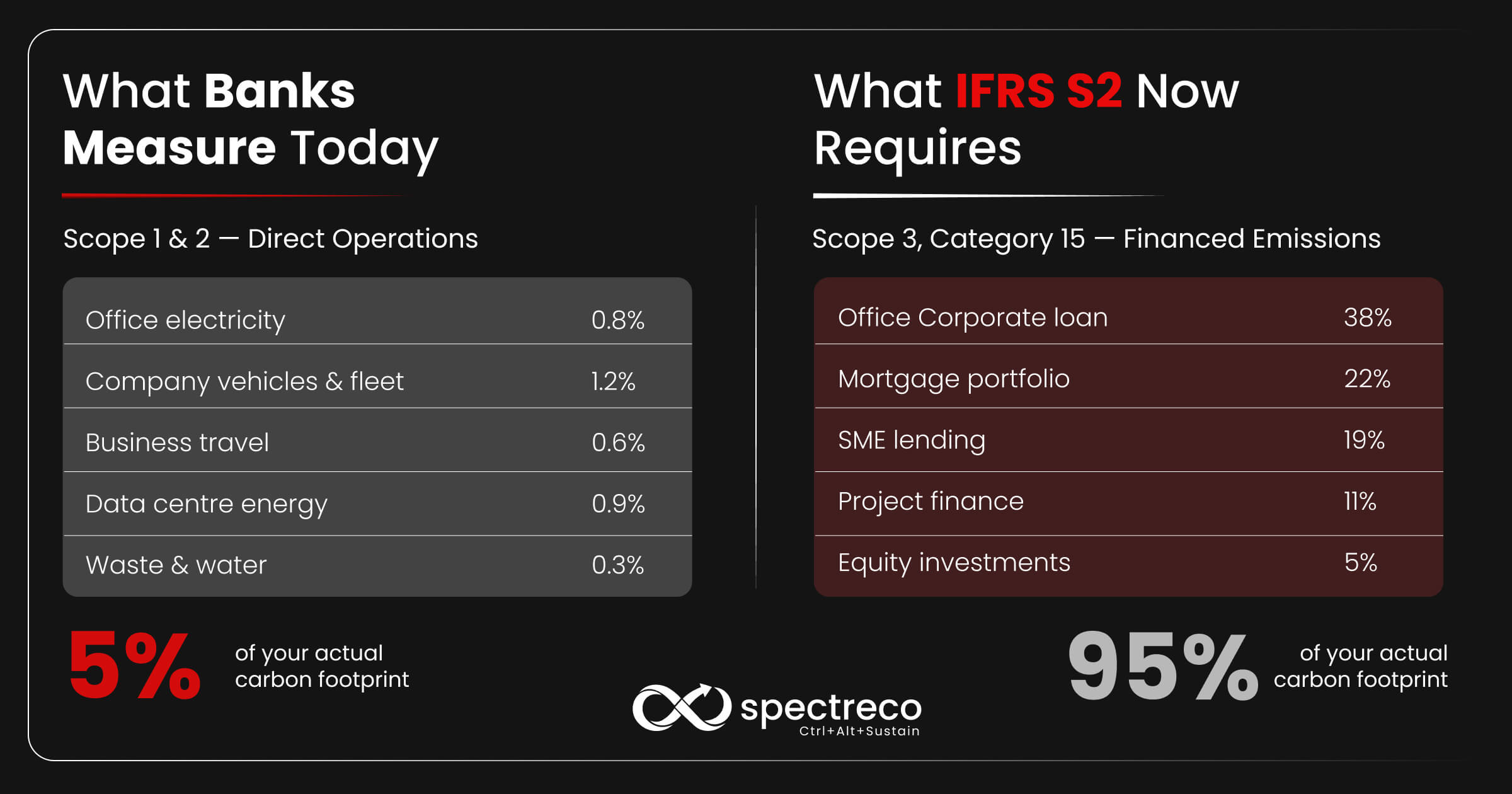

Ask the CFO of a large Pakistani commercial bank what their carbon footprint looks like, and most will point to electricity bills, office operations, and company vehicles.

Those numbers are almost irrelevant.

For a bank, the dominant source of greenhouse gas (GHG) emissions is not what happens inside its branches. It is what the bank finances: the loans it extends to textile mills, cement plants, fertiliser manufacturers, and energy projects. These are financed emissions, and for most financial institutions globally, they account for over 95% of their total carbon footprint.

The Securities and Exchange Commission of Pakistan (SECP) formally mandated IFRS S1 and IFRS S2 for all listed companies on 31 December 2024. Phase 1 large listed companies, including major commercial banks, must report for financial years beginning on or after 1 July 2025.

The first-year Scope 3 relief does not mean financed emissions can wait. Banks that do not build their measurement methodology in Year 1 will face a data gap in Year 2 they cannot close quickly. Borrower engagement, data collection, and PCAF methodology design take months. The time to start is now.

In April 2026, the SECP released an additional concept paper proposing that at least 70% of all ESG mutual fund investments flow into ESG-aligned assets, with formal consultation closing 21 April 2026. Pakistan's ESG regulatory pressure on financial institutions is not slowing down. It is accelerating.

What Are Financed Emissions and Why Do They Matter for Pakistani Banks?

Financed emissions are the GHG emissions of companies and projects that a bank finances through loans, bonds, or equity investments. They are classified as Scope 3 Category 15 under the GHG Protocol and disclosed under IFRS S2 paragraphs B58 to B63, which apply specifically to entities participating in asset management, commercial banking, and insurance activities.

The scale is the point. A bank's Scope 1 emissions (fuel combustion, company vehicles) and Scope 2 emissions (purchased electricity for branches) are typically small. Financed emissions are not. A single PKR 5 billion loan to a cement manufacturer can carry a larger GHG footprint than the bank's entire operational emissions for the year.

Pakistani banks are particularly exposed. The country's banking sector is heavily concentrated in loans to:

- Textiles: Pakistan's largest export sector, energy-intensive, predominantly coal and gas-fired

- Cement: one of the highest-emitting industries per tonne of output globally

- Fertilisers: ammonia-based production with significant Scope 1 process emissions

- Steel and metals: high coal consumption in integrated mills

- Energy generation: a mixed grid still dominated by fossil fuel generation

These sectors will drive the majority of any Pakistani bank's financed emissions inventory. They need to be prioritised first.

The State Bank of Pakistan (SBP) introduced its Environmental and Social Risk Management (ESRM) Manual and Green Banking Guidelines to address environmental risk in lending. These are important frameworks. But IFRS S2 goes further: it requires quantified GHG disclosure, not just risk management policy. Banks must satisfy both regulators.

Sources: PCAF, The Global GHG Accounting and Reporting Standard Part A: Financed Emissions, Third Edition, December 2025; SBP Green Banking Guidelines.

What Does SECP's IFRS S2 Mandate Actually Require from Pakistani Banks?

SECP's phased implementation structure applies to all listed companies and SECP-licensed non-listed Public Interest Companies. For banks, the timeline looks like this:

Sources: SECP IFRS S1/S2 mandate, 31 December 2024; IFRS Foundation Pakistan Jurisdictional Profile, July 2025.

Two things Phase 1 banks must disclose in their first sustainability report:

- Scope 1 and Scope 2 emissions: mandatory from Year 1. Covers direct emissions from bank operations and purchased electricity.

- Governance and strategy disclosures: board oversight of climate risk, scenario analysis, and transition plans.

Two things that are deferred but cannot be ignored:

- Scope 3 Category 15 financed emissions: exempt from mandatory disclosure in Year 1. Mandatory from Year 2. Banks that treat this as a Year 2 problem will not have audit-ready data when the obligation lands.

- Assurance: the SECP has proposed that companies obtain assurance on sustainability reporting from their auditors starting from the second year of reporting. Financed emissions data that was estimated loosely in Year 1 will not survive limited assurance review in Year 2.

The dual-regulator point: SECP governs IFRS S2 disclosure obligations for listed banks. SBP governs bank-specific reporting requirements through the ESRM Manual and Green Banking Guidelines. Compliance with SECP's IFRS S2 mandate does not automatically satisfy SBP requirements, and vice versa. Phase 1 banks need a reporting approach that addresses both.

.jpg)

How Do Pakistani Banks Actually Calculate Financed Emissions? The PCAF Standard Explained

PCAF (Partnership for Carbon Accounting Financials) is the global standard for calculating financed emissions. Founded in 2015 by Dutch financial institutions, PCAF has grown to over 670 financial institutions globally committed to measuring and disclosing portfolio GHG emissions. IFRS S2 references PCAF as the recommended methodology for financed emissions disclosure.

PCAF covers ten asset classes. Six are directly relevant to a typical Pakistani commercial bank's loan book:

Source: PCAF, The Global GHG Accounting and Reporting Standard Part A: Financed Emissions, Third Edition, December 2025.

PCAF scores data quality on a scale of 1 (best, borrower-reported verified data) to 5 (worst, sector-average estimates). Pakistani banks starting this work today will realistically score 4 to 5 on most asset classes. That is acceptable and expected for Year 1 baseline reporting.

The December 2025 PCAF update matters for Pakistani banks specifically. The updated Third Edition introduced new methodologies for use-of-proceeds structures including green bonds and sustainability-linked loans, sub-sovereign debt (relevant for government securities portfolios), and the option to report undrawn loan commitments in line with IFRS S1 and S2. Banks using the 2022 Second Edition are working from an outdated standard.

There is no Pakistani-specific PCAF adaptation yet. Banks will apply the global standard directly. The methodology is asset-class-based and data-quality-scored, which means even banks with limited borrower data can produce a defensible Year 1 baseline using sector averages, then improve data quality progressively.

Source: PCAF Third Edition, December 2025; PwC, PCAF Expands Financed Emissions Guidance and Introduces New Metrics, February 2026.

How Should a Pakistani Bank Start Measuring Financed Emissions Before the SECP Deadline?

Four steps, in order. This is the practical sequence for a Phase 1 bank that has not yet started.

- Map your loan book against PCAF asset classes. Identify which of the six primary PCAF categories apply to your portfolio. For most Pakistani commercial banks, the dominant categories will be business loans, project finance, listed equities, and commercial real estate. Complete this mapping before any data collection begins. Without it, you will collect the wrong data.

- Identify your highest-emission counterparties. Pakistan's banking sector is heavily concentrated in textiles, cement, steel, fertilisers, and energy generation. Run a simple exposure analysis: which borrowers represent the largest loan balances in carbon-intensive sectors? The top 20 to 30 counterparties will likely account for 80% or more of your total financed emissions. Start data collection there.

- Build your baseline emissions inventory using PCAF methodology. For counterparties where borrower-level emissions data is unavailable (which will be most cases in Pakistan initially), use PCAF's sector-average emission factors as the starting estimate. Document the PCAF data quality score assigned to each figure. A well-documented Score 4 or 5 disclosure is credible for Year 1. An undocumented estimate is not.

- Start borrower engagement now for Year 2. Improving data quality from Score 4 to Score 2 or 1 requires borrowers to share their Scope 1 and 2 emissions data directly. This takes relationship time. Build financed emissions data requests into your existing credit review and relationship management processes. Start with your ten largest exposures in high-emitting sectors. Do not treat this as a separate ESG project.

Spectreco's Virtual Sustainability Office (VSO) for banks without an internal ESG team

Frequently Asked Questions (FAQs)

The first-year Scope 3 exemption is not a reason to wait. It is a window to build the methodology, complete the loan book mapping, identify high-emission counterparties, and begin the borrower engagement that Year 2 mandatory disclosure will require.

Pakistan's ESG regulatory environment for financial institutions is moving faster than most banks have planned for. SECP's IFRS S2 Phase 1 deadline, the SBP's green banking framework, and the April 2026 ESG mutual fund proposal are three separate regulatory threads pulling in the same direction.

The banks that treat Year 1 as a learning year, not a free year, will be in a materially better position when financed emissions become auditable.

Spectreco works with financial institutions across Pakistan, the GCC, and the UK to build PCAF-aligned financed emissions inventories, stand up SECP IFRS S2 reporting workflows, and integrate ESG data into existing credit and risk processes. Book a 30-minute financed emissions readiness call with our Pakistan ESG team.

Book a Financed Emissions Readiness Call → spectreco.com

.jpg)

.jpg)

More From Our Blog

Your ESG Journey?