UAE ESG Compliance: What the 30 May 2026 Deadline Means for GCC Businesses | Spectreco

.jpg)

UAE ESG Compliance: What the 30 May 2026 Deadline Means for GCC Businesses

On 30 May 2025, the UAE became the first country in the MENA region to enforce climate-related corporate accountability through legislation. Federal Decree-Law No. 11 of 2024 on the Reduction of Climate Change Effects came into force, requiring every entity operating in the UAE to measure, report, and plan to reduce its greenhouse gas (GHG) emissions.

The full compliance deadline is 30 May 2026.

The penalties for non-compliance are not advisory. They range from AED 50,000 to AED 2,000,000 for first offences, doubling to AED 4,000,000 for repeat violations within two years.

For most companies operating across the GCC, this is not an isolated UAE problem. Qatar's central bank and financial regulator have mandated IFRS S1 and S2 for banks and regulated financial institutions from January 2026. Bahrain's CBB ESG reporting module is already operational. Saudi Arabia's Tadawul is moving from guidance to mandatory ISSB-aligned expectations. The GCC is becoming one of the most dynamic ESG compliance regions in the world, and 2026 is the year the enforcement cycle begins in earnest.

What Federal Decree-Law No. 11 of 2024 Actually Requires

The UAE Climate Law is not a disclosure framework. It is a legal obligation with enforceable penalties, overseen by the Ministry of Climate Change and Environment (MOCCAE).

The Three Core Obligations

Every in-scope entity must satisfy all three:

- Measurement: regular measurement of GHG emissions and preparation of an emissions inventory covering Scope 1 and Scope 2. Scope 3 reporting is anticipated from 2027, though this is not yet confirmed in law.

- Reporting: submission of periodic emissions reports through the national Measurement, Reporting and Verification (MRV) infrastructure, including the MOCCAE IEQT / mrv.ae platform, in formats and methodologies approved by MOCCAE.

- Reduction planning: submission of existing and planned GHG emissions reduction measures. The law does not specify fixed reduction targets by entity, but requires demonstrated active effort toward MOCCAE-set annual reduction targets.

Records of measured emissions must be maintained for a minimum of five years and must be accessible to regulators on request.

Who Is in Scope

No minimum threshold. No sector exemption. The law applies to all public and private entities including those operating in free zones and state-owned enterprises. If your UAE operations produce GHG emissions, you are in scope.

Free zone status provides no insulation. DIFC and ADGM financial services firms, JAFZA manufacturers, DMCC commodity traders, and Dubai Internet City technology companies are all subject to the same law as mainland entities.

Large Emitters: Accelerated Obligations

Entities emitting 0.5 million metric tonnes or more of CO2 equivalent per year (Scope 1 and Scope 2 combined) face additional requirements under Cabinet Resolution No. 67 of 2024:

- Registration with the National Carbon Credit Registry (NRCC)

- GHG inventory aligned with ISO 14064

- Third-party verification from a MOCCAE-approved verifier

- Independent verification of 2026 reporting year data required from 2027 under the Abu Dhabi MRV system

One Caveat on the Deadline

Ropes and Gray noted in April 2026 that MOCCAE representatives have indicated the 30 May 2026 deadline may be extended, pending issuance of technical guidance still under development. A revised compliance date has not been confirmed.

Plan for 30 May 2026. Treat any extension as a bonus, not a plan.

Sources: PwC UAE, UAE Climate Change Law — Mandatory Emissions Reporting Obligations, November 2025; Ropes and Gray, Preparing for New UAE GHG Emissions Reporting and Reduction Requirements, April 2026; Zevero, UAE Climate Law Explained, 2026.

What Are the Penalties and Who Enforces Them?

The Penalty Structure

What happens if a UAE company misses the 30 May 2026 GHG reporting deadline? Non-compliance with Federal Decree-Law No. 11 of 2024 carries administrative fines of AED 50,000 to AED 2,000,000 for first offences. Repeat violations within two years of a prior conviction can double the penalty to AED 4,000,000.

Additional consequences beyond financial penalties:

- Exclusion from UAE government procurement

- Temporary suspension of operations

- Mandatory corrective orders issued without court proceedings

Who Enforces It

Enforcement is not limited to MOCCAE. The Securities and Commodities Authority (SCA) and the Central Bank of the UAE (CBUAE) operate overlapping ESG disclosure rules for financial institutions. For listed companies and financial services firms, non-compliance can trigger action from multiple regulators simultaneously.

Two enforcement mechanisms already operational:

- MOCCAE and authorised bodies conduct inspections, audits, and issue mandatory corrective orders

- The Abu Dhabi Environment Agency runs its own MRV system with independent verification requirements starting in 2027 for reporting year 2026

The Free Zone Assumption Is Wrong

Many multinationals assume free zone status provides regulatory insulation. It does not. The law explicitly captures all entities in UAE free zones. DIFC and ADGM financial services firms face the UAE Climate Law alongside growing sustainability disclosure expectations from institutional investors and international clients.

Sources: Ropes and Gray, April 2026; RMC Consultancy, UAE Climate Law 2026 ISO 14064 Guide, March 2026; SustainGulf, UAE Climate Law, January 2026.

Qatar, Bahrain, and the Wider GCC: The Multi-Regulator Compliance Picture

The UAE deadline is the most urgent, but it is not the only one. Across the GCC, ESG and climate reporting frameworks moved from voluntary guidance to mandatory obligation in 2025 and 2026.

GCC Regulatory Timeline at a Glance

Sources: QCB Sustainability Reporting Framework (SRF); QFCRA GENE Rules 2025; CBB ESG Reporting Module; Sustaingulf, Corporate Sustainability Reporting in the Gulf, December 2025; HLB AG, QCB ESG Rules in Qatar, March 2026.

Three Facts That Define the Multi-Jurisdiction Compliance Challenge

- Qatar uses dual regulators. The Qatar Central Bank (QCB) governs banks. The Qatar Financial Centre Regulatory Authority (QFCRA) governs QFC-authorised firms including banks and insurers under the GENE Rules 2025. A financial institution operating in Qatar may be subject to both frameworks simultaneously.

- The standards are aligned but not identical. Qatar's QCB and QFCRA both mandate IFRS S1 and S2. The UAE Climate Law mandates GHG reporting under MOCCAE's own MRV methodology, which references international standards including ISO 14064 as an accepted framework but operates as a separate system from ISSB. A company that is IFRS S2 compliant in Qatar is not automatically UAE Climate Law compliant.

- Sustainable bond markets are accelerating the pressure. According to S&P Global, sustainable bond issuance in the Middle East increased approximately 3% in 2025, even as global sustainable bond volumes fell 21%. The GCC is on track for USD 20 to 25 billion in sustainable bond issuance in 2026. Capital market access increasingly depends on credible ESG disclosure.

Source: S&P Global Sustainable Finance, GCC sustainable bond market outlook, 2026.

Why Siloed Processes Will Not Work Across GCC Jurisdictions

Most companies operating across the GCC have built their ESG reporting in silos: one team handles UAE sustainability reports, another handles Qatar investor disclosures, another manages group-level IFRS S2 for a European parent.

The 2026 regulatory environment breaks that model. Four reasons:

The UAE Requires Facility-Level Data

Not group-level estimates allocated to UAE operations. MOCCAE wants entity-specific data submitted through the mrv.ae platform. That data must be built from UAE operational sources, not downloaded from a group emissions model.

Qatar's IFRS S1 and S2 Needs More Than Emissions Data

IFRS S2 requires four-pillar disclosures: governance, strategy, risk management, and metrics. A UAE GHG inventory satisfies the metrics component. It does not produce a complete IFRS S2 report. The governance and strategy pillars require board-level documentation, scenario analysis, and financial impact quantification that a GHG inventory alone cannot generate.

Verification Timelines Are Converging

The UAE Abu Dhabi MRV system requires third-party verification from 2027. Qatar's QCB intends to develop a parallel assurance framework. Companies need data systems that can support verification from multiple accreditation bodies, not just a single auditor.

The Window to Build Unified Infrastructure Is Closing

Building separate compliance processes for UAE, Qatar, Bahrain, and eventually Saudi Arabia means duplicating data collection, duplicating verification, and duplicating cost. A unified GHG and ESG data platform built now can serve all four frameworks from one data source. Built in 2027, it costs more and starts behind.

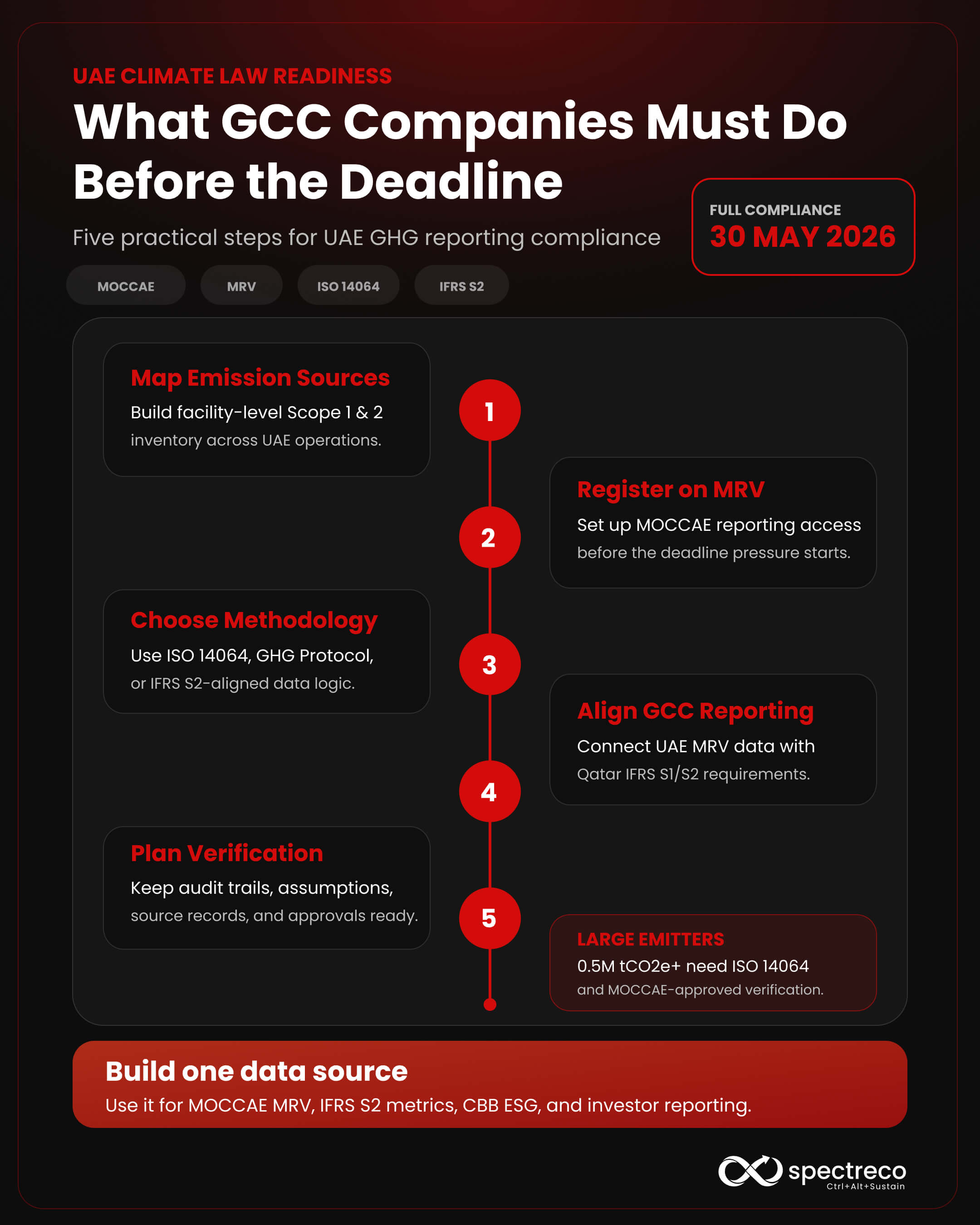

What GCC Companies Must Do Before the Deadline

Five steps, in order. Applicable to any company with UAE operations in scope of the Climate Law.

- Map your emissions sources across UAE facilities. Build a complete inventory of all Scope 1 and Scope 2 emission sources: fuel combustion, process emissions, purchased electricity, cooling and steam. Do this at facility level, not group level. The MOCCAE reporting system requires entity-specific data, not allocations.

- Register on the MOCCAE MRV platform (mrv.ae). MOCCAE's national MRV infrastructure is the mandatory submission channel under the Climate Law. Companies need to register their entities and emission sources on the platform now. Waiting until the deadline to set up a new platform account and learn the submission format creates unnecessary compliance risk.

- Decide on your GHG measurement methodology. MOCCAE accepts ISO 14064 as an approved methodology. Companies with existing GHG programmes built on ISO 14064, the GHG Protocol, or IFRS S2 methodology have a head start. Companies with no existing emissions measurement need to build a baseline inventory from scratch using 12 months of operational data (utility bills, fuel records, production logs).

- Align your UAE and Qatar reporting processes. If your organisation is also in scope for Qatar's QCB or QFCRA frameworks, map the MOCCAE Scope 1 and Scope 2 data against IFRS S2's metrics pillar disclosure requirements now. The emissions data overlaps significantly. The reporting format and governance requirements do not. Build both from a shared data source rather than two separate collection exercises.

- Plan for verification. Large emitters (0.5 million tonnes CO2e or above) need a MOCCAE-approved third-party verifier now. All entities should design their data systems with audit trails from the start: source data traceability, documented methodology, recorded assumptions. Systems built without audit trails will need to be rebuilt before the verification requirements arrive in 2027.

Spectreco's Virtual Sustainability Office (VSO) for GCC companies without internal ESG capability

Spectreco's Climate and Green Finance advisory for UAE Climate Law compliance strategy

Frequently Asked Questions (FAQs)

The GCC is not a single ESG compliance jurisdiction. It is six separate regulatory environments converging on the same 2026 timeline, with different frameworks, different enforcement bodies, and different reporting platforms.

The companies that manage this well are the ones that treat their GHG measurement infrastructure as a shared asset across jurisdictions: one source of emissions data feeding MOCCAE MRV reporting, IFRS S2 metrics disclosure, CBB ESG reporting, and investor-facing sustainability reports simultaneously.

The companies that will struggle are the ones still building separate processes for each framework as each deadline arrives.

Are your GCC operations ready for the 30 May UAE Climate Law deadline and the 2026 ISSB-based reporting cycle? Spectreco works with financial services, real estate, and corporate clients across the GCC to build MOCCAE-compliant GHG reporting infrastructure, IFRS S1/S2 disclosure programmes, and multi-jurisdiction ESG data platforms. If you are still building your reporting processes, contact the Spectreco GCC team for a 30-minute compliance gap assessment.

Book a GCC ESG Compliance Gap Assessment → spectreco.com

.jpg)

.jpg)

More From Our Blog

Your ESG Journey?