Oman MSX ESG & ISSB Reporting: What Listed Companies Must Do

Oman ESG & ISSB Reporting: What MSX-Listed Companies Must Do in 2026

If you are a CFO or Company Secretary at a Muscat Stock Exchange (MSX) listed company, ESG reporting is no longer a choice you get to make. It is a filing obligation, and the bar is about to rise again. Oman has already made standalone ESG disclosure mandatory for every listed public joint-stock company (SAOG), and in early 2026 the Financial Services Authority (FSA) formally adopted IFRS S1 and IFRS S2, the global sustainability and climate disclosure standards. This article sets out the Oman MSX ESG ISSB reporting picture for listed companies in 2026: what is mandatory now, what is coming, and the gap most boards have not yet closed.

Spectreco, an ESG technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore, works with financial services, energy, and industrial clients across all six GCC markets. We have mapped the Oman position against the neighbouring UAE, Saudi, Qatar, Bahrain, and Kuwait frameworks so you can see exactly where the Sultanate sits, and what your reporting team should be building right now.

Is ESG Reporting Mandatory for MSX-Listed Companies?

Yes. ESG reporting is mandatory for all SAOGs listed on the Muscat Stock Exchange. Administrative Decision 77/2025, published in June 2025, requires listed public joint-stock companies to disclose their ESG practices on the MSX platform and on their own website. The first mandatory standalone reports, built on 30 GRI-based metrics, were due by 31 March 2025.

Sources: Trowers & Hamlins, Oman implements compulsory ESG reporting (June 2025); Glass Lewis, Gulf Exchanges Encourage ESG Disclosures.

The MSX and CMA ESG Framework: 30 Metrics, Now Mandatory

The MSX, under the Capital Market Authority (CMA), issued Oman's first detailed ESG Disclosure Guidelines in 2023. The framework sets out 30 metrics split across the three pillars: environmental, social, and governance. It is aligned with the Unified GCC ESG Disclosure Metrics for Listed Companies, published in 2022, and built on the Global Reporting Initiative (GRI) Universal Standards. GRI is the global standard for reporting an organisation's impact on society and the environment.

Source: Glass Lewis, Gulf Exchanges Encourage ESG Disclosures for GCC Listed Companies.

What Changed: From Voluntary to a Standalone Filing

For 2023 activities, reporting was voluntary. From 2025, it became mandatory. SAOGs must now publish a standalone ESG report, separate from the annual financial report, prepared in line with the GRI Universal Standards and covering the 30 metrics. The report must be accessible on the company website, and disclosures are filed through a dedicated MSX ESG Disclosures Platform.

The MSX requirement is explicit on one point that catches reporting teams out: both positive and negative ESG information must be presented accurately. Selective or flattering disclosure is a compliance failure. Companies that get it wrong face fines and escalation to the FSA, and greenwashing or the omission of material risk can trigger regulatory and reputational consequences.

Source: Trowers & Hamlins, Oman implements compulsory ESG reporting.

The FSA Has Adopted IFRS S1 and S2: What It Means for Listed Companies

This is the development that changes the trajectory. By Decision E/7/2026, published in the Official Gazette in early 2026, the FSA formally adopted IFRS S1 and IFRS S2 for the preparation and audit of financial and sustainability reports of listed public joint-stock companies and financial institutions. IFRS S2 (Climate-related Disclosures) is the ISSB climate standard issued in June 2023. IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) is its broader companion.

Sources: Trowers & Hamlins, Oman adopts IFRS Sustainability Disclosure Standards (April 2026); Decree.om, FSA Adopts IFRS S1 and IFRS S2.

The decision moves sustainability disclosure out of the standalone, impact-narrative box and into the core regulatory reporting framework, the same place financial statements already sit. That reframing matters for boards, finance functions, and auditors, because IFRS S1 and S2 are built on financial materiality: how sustainability and climate risk affect the company's prospects, cash flows, and cost of capital, not only how the company affects the world. In practice it pulls sustainability data toward the finance function, which is why many GCC issuers are now formalising an ESG controller role to own that data with the same rigour as financial reporting.

The Real Timeline: 2029, Not 2026

Here is the point every Omani reporting team needs to be clear on, because it is widely misstated. The FSA adopted a phased timetable. IFRS S1 and IFRS S2 must be fully applied from 1 January 2029. The one carve-out is Scope 3 greenhouse gas emissions under IFRS S2, which become mandatory from 1 January 2030. Scope 3 covers all other indirect emissions across the value chain. The transition is expected to begin from the 2027 reporting cycle, with companies encouraged to run gap analyses and strengthen governance before full adoption.

Sources: Trowers & Hamlins (April 2026); Oman Observer, Oman moves towards mandatory sustainability disclosures (May 2026).

Treating 2029 as distant is the trap. IFRS S2 requires four pillars of disclosure: governance, strategy, risk management, and metrics and targets. The metrics pillar leans on a clean Scope 1 and Scope 2 emissions inventory built on the GHG Protocol. The governance and strategy pillars require board-level documentation, scenario analysis, and quantified financial impact that no spreadsheet produces overnight. Companies that wait until 2028 to start will be building three years of capability in one.

The FSA also attached teeth. Non-compliance can draw administrative penalties, including a warning, suspension from practice for up to two years, and striking off from the Accountants and Auditors Register.

Source: Trowers & Hamlins, Oman adopts IFRS Sustainability Disclosure Standards.

Why This Sits Inside Oman Vision 2040

None of this is regulation for its own sake. Oman Vision 2040 places economic diversification away from oil and a credible sustainability agenda at the centre of national strategy, and it commits Oman to net zero carbon emissions by 2050. The country's updated net-zero roadmap notes total greenhouse gas emissions of roughly 94 million tonnes of CO2 equivalent in 2024, projected to rise to about 127 million tonnes by 2050 without intervention, alongside a target to lift renewable electricity sharply through to 2040.

Sources: Oman Vision 2040 national programmes; ChemAnalyst, Oman Updates Net-Zero Emissions Strategy for 2050 (May 2026).

For a listed SAOG, the link is direct. Decision-useful ESG data is how Oman attracts the foreign direct investment and green capital Vision 2040 depends on. Spectreco CEO highlighted the same shift publicly when speaking to Arab News in 2025, noting that Oman had already made ESG reporting mandatory while several neighbours were still moving toward it.

Source: Arab News, AI-led Shariah-compliant ESG Index (April 2025).

How Oman Compares to the Rest of the GCC

The GCC is not one ESG jurisdiction. It is six regulatory environments converging on ISSB as a common language while diverging on scope, timing, and enforcement. Oman and Bahrain anchor their current requirements in GRI; Qatar and Kuwait have moved earliest on explicit ISSB adoption; the UAE layers a federal climate law over securities-regulator reporting. The table below sets out where each market stands.

Sources: Oren, GCC ESG Regulations Guide 2026; Spectreco, UAE ESG Compliance and the 30 May 2026 Deadline; Deloitte IAS Plus, ISSB adoption by jurisdiction.

The practical takeaway for any company with operations in more than one Gulf market: build the GHG and ESG data layer once, then feed it into each jurisdiction's format. Oman's GRI report, a Qatar IFRS S2 disclosure, and a UAE MOCCAE submission can all draw from a single source of emissions data. Building them in silos triples the cost. For the full UAE picture, see our UAE ESG compliance pillar, and for the Saudi position, our Saudi Arabia ISSB reporting guide.

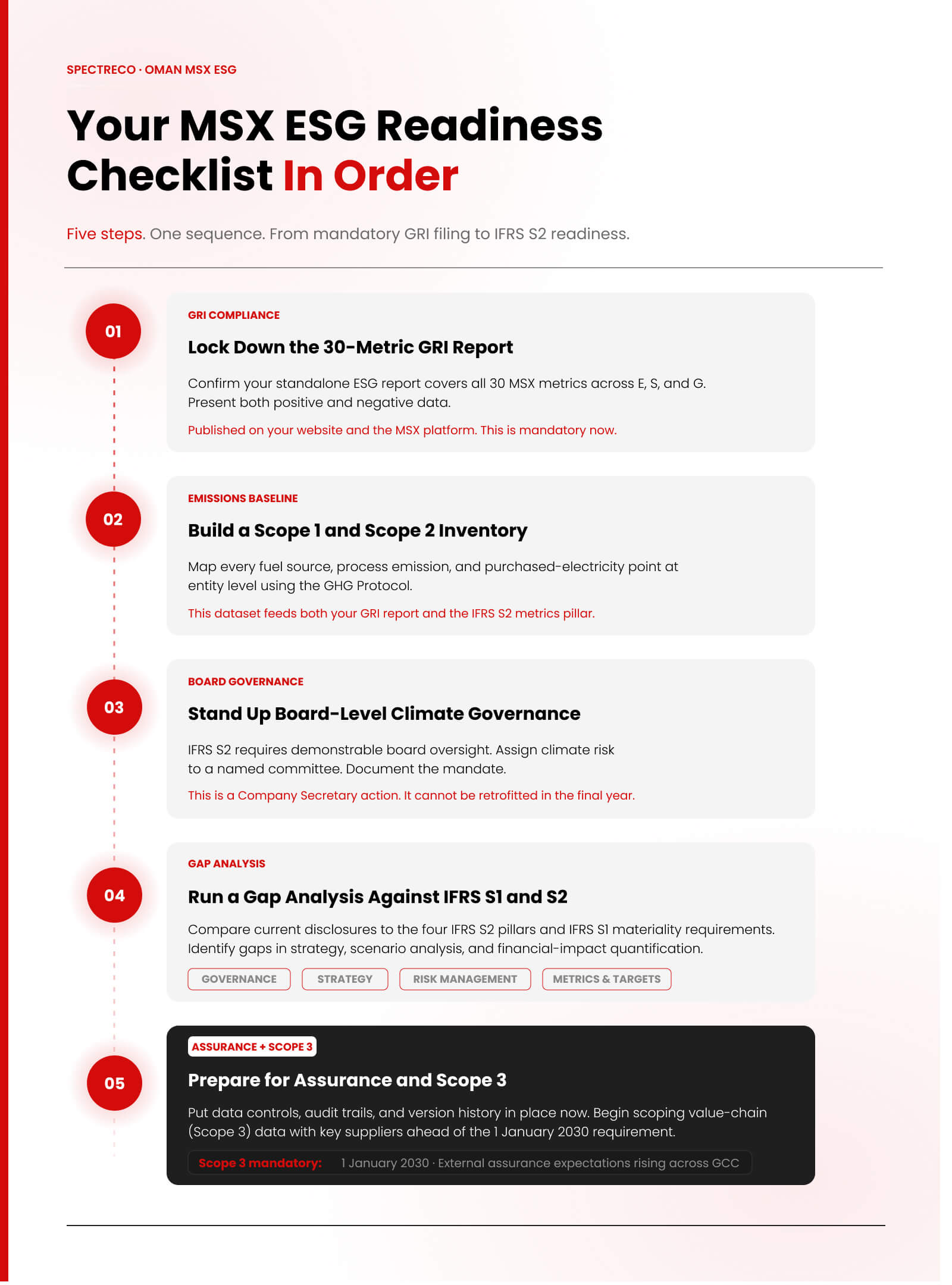

How to Get MSX ESG and ISSB Ready: A 5-Step Checklist

These five steps move a SAOG from a compliant GRI filing today to an IFRS S1 and S2 capable function before 2029. Order matters.

- Lock down the 30-metric GRI report. Confirm your current standalone ESG report covers all 30 MSX metrics across E, S, and G, presents both positive and negative data, and is published on your website and the MSX platform. This is the baseline you are already obligated to meet.

- Build a Scope 1 and Scope 2 emissions inventory. Map every fuel source, process emission, and purchased-electricity point at entity level using the GHG Protocol. This single dataset feeds both your GRI report and the IFRS S2 metrics pillar. Do not wait for the 2029 date to start.

- Stand up board-level climate governance. IFRS S2 requires demonstrable board oversight. Assign climate risk to a named committee, document the mandate, and set a reporting cadence. This is a Company Secretary action, and it cannot be retrofitted in the final year.

- Run a gap analysis against IFRS S1 and S2. Compare your current disclosures to the four IFRS S2 pillars and the IFRS S1 materiality requirements. Identify what is missing in strategy, scenario analysis, and financial-impact quantification, then build a phased plan toward the 2027 transition cycle.

- Prepare for assurance and Scope 3. External assurance expectations are rising across the GCC. Put data controls, audit trails, and version history in place now, and begin scoping value-chain (Scope 3) data with key suppliers ahead of the 1 January 2030 requirement.

Frequently Asked Questions (FAQs)

Where Spectreco Fits

Oman has moved faster than most of its neighbours on mandatory ESG, and the IFRS S1 and S2 clock is now running toward 2029. The companies that absorb the next standard without disruption are the ones building the data and governance infrastructure in 2026, not 2028.

Spectreco helps MSX-listed banks, energy companies, and industrials build that infrastructure: GRI-compliant ESG reports, a clean Scope 1 and 2 inventory, board-level climate governance, and an IFRS S1 and S2 readiness plan that serves Oman and every other GCC market you operate in. To start, book a GCC ESG compliance gap assessment with our team through Spectreco's Compliance, Reporting & Disclosures advisory.

.jpg)

.jpg)

More From Our Blog

.jpg)

.jpg)

Your ESG Journey?