SECP IFRS S2: Complete Compliance Guide for Pakistan 2026

SECP IFRS S2: The Complete Compliance Guide for Pakistan Listed Companies

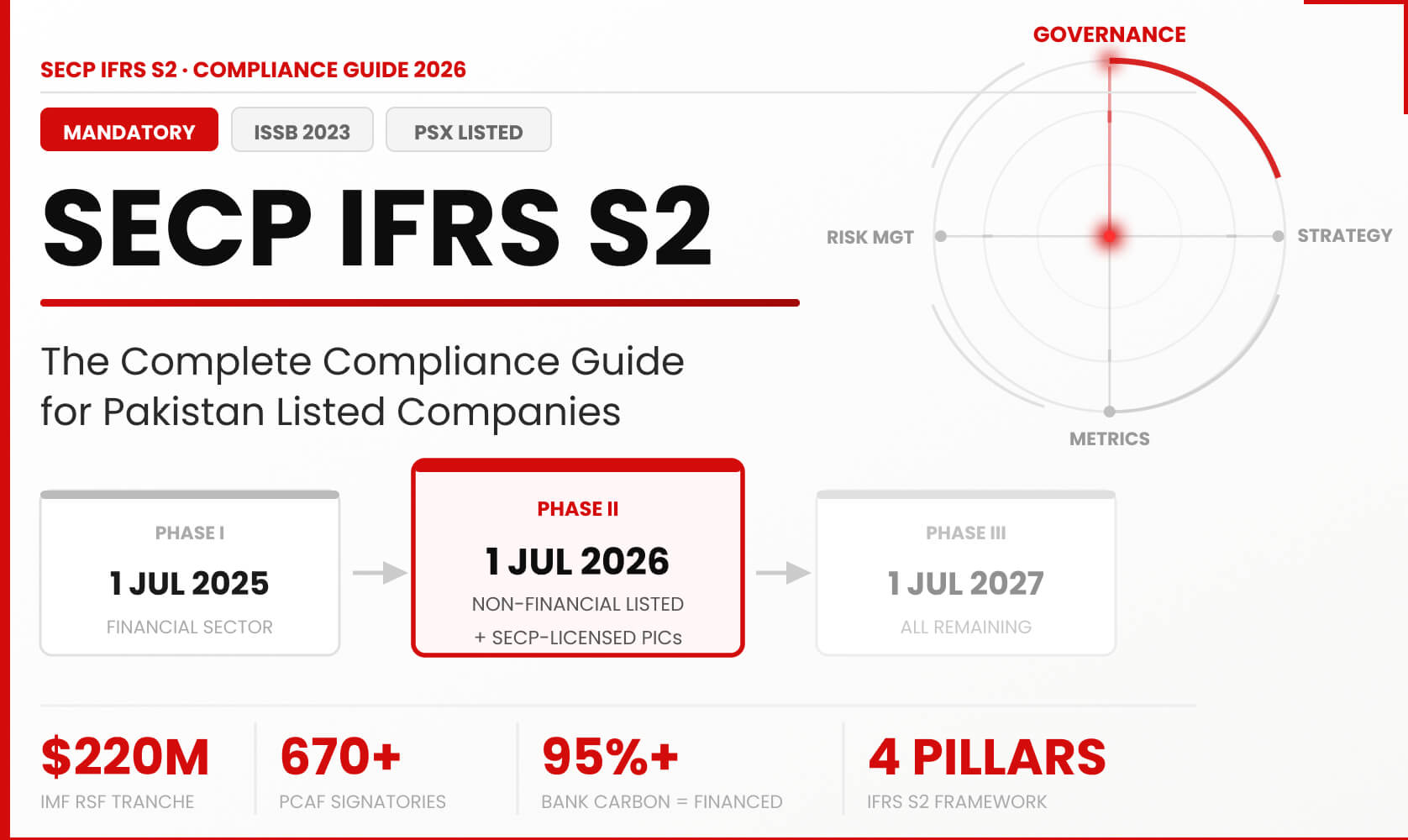

The Securities and Exchange Commission of Pakistan (SECP) issued its sustainability reporting mandate on December 31, 2024, making IFRS S1 and IFRS S2 mandatory for all Pakistan Stock Exchange (PSX)-listed companies and SECP-licensed non-listed Public Interest Companies (PICs). The first phase has already begun. Phase 2, which covers non-financial listed companies and licensed PICs above a defined size threshold, takes effect for annual reporting periods beginning on or after July 1, 2026.

That deadline is not a proposal. It is a legal obligation under Section 238 of the Companies Act 2017.

This guide covers what IFRS S2 requires, who is in scope for Phase 2, how the four disclosure pillars work in practice, what financed emissions mean for Pakistani banks, how the IMF climate facility connects to corporate ESG compliance, and what a seven-step readiness process looks like from the boardroom down.

Contents

- The SECP Mandate: What Changed on December 31, 2024

- Phase 1, Phase 2, and Phase 3: Who Is In Scope and When

- What Does SECP IFRS S2 Actually Require?

- Scope 1, Scope 2, and Scope 3 Under SECP Rules

- Financed Emissions for Pakistani Banks: PCAF and Category 15

- The IMF RSF Tranche: Why ESG Compliance Has a Balance-of-Payments Dimension

- 7-Step SECP IFRS S2 Readiness Checklist

- Frequently Asked Questions

The SECP Mandate: What Changed on December 31, 2024

Before December 31, 2024, Pakistan had ESG disclosure guidelines for listed companies issued on June 12, 2024, but they were voluntary. Companies could adopt IFRS Sustainability Standards or ignore them. That changed with a single notification issued under Section 238 of the Companies Act 2017.

The SECP issued a formal Order mandating the phase-wise adoption of the International Sustainability Standards Board (ISSB) Sustainability Disclosure Standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures). These two standards were issued by the ISSB in June 2023 and have since been adopted in over 21 jurisdictions including Australia, Brazil, Chile, Mexico, Hong Kong, Qatar, and Nigeria.

Source: IFRS Foundation, Pakistan Jurisdictional Profile . SECP Order, December 31, 2024 (Section 238, Companies Act 2017) .

Pakistan is now formally part of that group.

The SECP also launched the 'ESG Sustain' platform to centralise corporate sustainability disclosures, signalling that the regulator intends to monitor compliance, not just mandate it. The State Bank of Pakistan (SBP) is a parallel actor in this landscape, particularly for climate-related risk disclosures in the banking sector. For the structural challenges facing Pakistani companies in meeting these requirements, The News International offers a detailed assessment.

Companies that were already filing voluntary sustainability reports have a head start. The majority of PSX-listed non-financial companies have not yet built the governance structures, data systems, or assurance-ready reporting processes IFRS S2 demands.

Phase 1, Phase 2, and Phase 3: Who Is In Scope and When

The SECP phased the mandate by company size, not by sector. A company qualifies for a given phase if it meets any two of three thresholds: annual turnover, employee headcount, or total assets.

Source: SECP Order under Section 238, Companies Act 2017, notified December 31, 2024 . Moore Shekha Mufti, Sustainability Reporting Order Memorandum, February 2025 .

What Phase 2 Means in Practice

A PSX-listed cement manufacturer with turnover above Rs. 12.5 billion and a workforce above 500 is in Phase 2. So is a listed textile exporter with total assets above Rs. 6.25 billion and turnover above Rs. 12.5 billion. The thresholds are cumulative across the company's last two consecutive financial years, reducing the risk that a single exceptional year triggers early compliance.

SECP-licensed non-listed PICs in Phase 2 include non-banking finance companies (NBFCs), modarabas, and SECP-registered microfinance institutions that meet the size criteria above. These entities are not listed on PSX but carry public interest obligations that place them within the SECP regulatory perimeter.

One practical detail often missed: the Scope 3 emissions disclosure obligation does not start in Year 1 of reporting. SECP allows companies to introduce Scope 3 reporting from their second year, easing the data collection burden in the first reporting cycle. Similarly, assurance by auditors becomes mandatory from the second year of reporting, not the first.

Phase 2 Critical Note: Scope 3 emissions and external assurance are both deferred to Year 2 of reporting. Year 1 focuses on Scope 1, Scope 2, governance disclosures, and strategy. The sustainability report must be included in the annual report, after the directors' report, unless it is submitted separately within nine months of the financial year-end.

What Does SECP IFRS S2 Actually Require?

IFRS S2 (Climate-related Disclosures) is structured around four content pillars, which Pakistan adopted directly from the Task Force on Climate-related Financial Disclosures (TCFD) framework. The TCFD is the voluntary global framework covering governance, strategy, risk management, and metrics and targets that has been largely superseded by IFRS S2 as the mandatory standard.

Pillar 1: Governance

The governance pillar requires disclosure of how the board and management oversee climate-related risks and opportunities. This is not a tick-box exercise. SECP expects named bodies: which board committee holds responsibility, what qualifications that committee has, how frequently climate risk is reviewed at board level, and how executive remuneration is linked to climate-related targets where applicable.

The key test is whether your governance disclosures would satisfy an institutional investor conducting climate due diligence. Vague references to 'board oversight of ESG matters' do not pass that test.

Pillar 2: Strategy

Strategy disclosure requires companies to explain how climate-related risks and opportunities affect their business model, financial planning, and strategy across short, medium, and long-term horizons. IFRS S2 mandates climate scenario analysis: companies must demonstrate they have tested their business against at least two climate pathways.

For Pakistani companies, this means modelling the financial effects of physical risks (flooding, heat stress, water scarcity, which are all acutely relevant given Pakistan's climate vulnerability) alongside transition risks (carbon pricing, regulatory tightening, changing customer demand as the economy decarbonises).

The IMF's 2023 Climate Public Investment Management Assessment (C-PIMA) of Pakistan identified disaster risk management, water use efficiency, and climate-related financial disclosure as the three structural priorities for the country. Strategy disclosures under IFRS S2 address the third directly. See IMF Country Report No. 25/109 for the full programme detail.

Pillar 3: Risk Management

Risk management disclosures explain the processes a company uses to identify, assess, and manage climate-related risks, and how those processes are integrated into the overall enterprise risk management framework. SECP does not want a standalone ESG risk register. It wants evidence that climate risk sits inside the same governance structure as financial and operational risk.

For listed companies in sectors like textiles, cement, sugar, and fertilisers, where physical climate exposure and transition regulatory risk are both material, this pillar requires substantive process documentation, not narrative summary.

Pillar 4: Metrics and Targets

The metrics and targets pillar is where quantitative disclosure requirements concentrate. Under IFRS S2, companies must disclose:

- Absolute Scope 1 and Scope 2 greenhouse gas (GHG) emissions, expressed in metric tonnes of CO2 equivalent (tCO2e)

- Industry-specific metrics drawn from the Sustainability Accounting Standards Board (SASB) standards, which IFRS S2 incorporates through its Appendix B across 11 sectors and 70+ industries

- Quantified climate-related targets and the progress made against them

- Cross-industry metrics including energy consumption, water, waste, and capital deployment toward climate-related opportunities

The SECP requirement also references IFRS S2 paragraph 29, which mandates disclosure of the methodology used to measure GHG emissions. The GHG Protocol is the globally accepted methodology, and Pakistan has adopted it as the baseline standard for Scope 1 and Scope 2 measurement.

Scope 1, Scope 2, and Scope 3 Under SECP Rules

The three scopes of GHG emissions define the boundary of what companies must measure and report. Understanding which applies in Year 1 versus Year 2 of SECP compliance is critical for sequencing your data infrastructure correctly.

Scope 1: Direct Emissions

Scope 1 covers all direct GHG emissions from sources owned or controlled by the entity. For a Pakistani cement manufacturer, Scope 1 includes kiln fuel combustion. For an airline listed on PSX, Scope 1 is jet fuel burned by owned aircraft. For a bank, Scope 1 is typically small: generator diesel at branches and fuel in the company fleet.

Scope 1 is mandatory from Year 1 for all Phase 1 and Phase 2 companies. Data sources include fuel purchase records, utility bills for captive generation, and process measurement for industrial companies.

Scope 2: Purchased Energy Emissions

Scope 2 covers indirect emissions from purchased electricity, heat, steam, or cooling. For most Pakistan Stock Exchange-listed companies, Scope 2 is dominated by grid electricity consumption. Pakistan's national electricity grid has a significant coal and furnace oil component, making Scope 2 emissions material for any energy-intensive business.

The GHG Protocol requires companies to use the local grid emission factor published by the National Electric Power Regulatory Authority (NEPRA) or the applicable market-based factor if renewable energy certificates are in use. This detail matters for auditors assessing first-year SECP compliance.

Scope 3: Value Chain Emissions

Scope 3 covers all other indirect emissions across the value chain, including upstream raw materials, downstream use of sold products, employee commuting, business travel, and, for financial institutions, the critical Category 15 financed emissions. Scope 3 is deferred to Year 2 under SECP's phased implementation.

For non-financial companies, Scope 3 Category 1 (purchased goods and services) often represents the largest share of total emissions. A Pakistani textile exporter buying cotton, chemicals, and energy-intensive yarn has substantial upstream emissions that will need to be disclosed once the Year 2 obligation begins.

Financed Emissions for Pakistani Banks: PCAF and Category 15

For banks, the emissions picture is fundamentally different from that of an industrial company. The Partnership for Carbon Accounting Financials (PCAF) is the global standard for measuring GHG emissions associated with loans, bonds, and equity investments. These are classified as Scope 3 Category 15 under the GHG Protocol.

The reason Category 15 dominates the banking sector's carbon footprint is straightforward. A bank's direct operations: its offices, ATMs, and branch network, account for less than 5% of its total GHG inventory. The other 95% or more of a bank's carbon exposure sits in the loans and investments it holds on its balance sheet. A commercial bank financing coal power infrastructure, a petrochemical plant, or a fleet of heavy vehicles carries the carbon intensity of those activities as financed emissions.

Source: PCAF Global GHG Accounting and Reporting Standard for the Financial Industry, v3, December 2025 . PCAF has over 670 financial institution signatories globally. See also: Resources Future, Financed Emissions Explained: What Banks Must Know, June 2025 .

How PCAF Works for Pakistani Banks

PCAF provides methodology across ten asset classes, including listed equities, corporate bonds, business loans and lines of credit, project finance, commercial real estate mortgages, and sovereign debt. For each asset class, PCAF specifies an attribution factor (the bank's share of total outstanding debt or equity in the borrower) and a data quality score on a scale of 1 to 5, where 1 represents verified, borrower-specific data and 5 represents estimates based on sector averages.

For a Pakistani bank with corporate loan exposure to energy, real estate, and manufacturing sectors, the first step in PCAF implementation is an asset-class inventory covering the bank's full lending portfolio. This is not a data exercise that can be completed in weeks. Banks that have not yet begun should treat this as a six-to-twelve-month programme.

IFRS S2 paragraph 29(a)(vi) specifically references PCAF as the applicable methodology for financed emissions disclosure. This connection between IFRS S2 and PCAF is not optional for Pakistani banks: it is the required calculation standard under the mandate the SECP issued on December 31, 2024. For a detailed walkthrough of PCAF methodology and financed emissions calculation by asset class for Pakistani financial institutions, read Financed Emissions Explained: What Pakistani Banks Must Know.

The State Bank of Pakistan has been actively engaged in climate finance reform as part of the IMF's Resilience and Sustainability Facility (RSF) conditions. SBP's own climate risk guidelines for banks reference both IFRS S2 and financed emissions measurement, creating alignment between the banking regulator and the SECP mandate

The IMF RSF Tranche: Why ESG Compliance Has a Balance-of-Payments Dimension

In May 2025, the IMF Executive Board approved Pakistan's first arrangement under the Resilience and Sustainability Facility (RSF), alongside the first review of Pakistan's Extended Fund Facility (EFF). The RSF was explicitly linked to climate resilience reforms, including improvements to climate-related financial disclosure by banks and corporates. See IMF Press Release No. 25/137 for the full terms.

By December 2025, the IMF completed the second review of the EFF and the first review of the RSF, releasing approximately $200 million under the climate facility (IMF Press Release No. 25/411). In May 2026, Pakistan received a further disbursement of approximately $220 million under the RSF as part of a combined $1.3 billion tranche from the IMF. Total disbursements under both programs reached approximately $4.8 billion.

Source: IMF Press Release No. 25/137, May 2025 . IMF Press Release No. 25/411, December 2025 . Arab News: Pakistan central bank receives $1.3 billion IMF disbursement, May 2026 .

The RSF conditions explicitly include strengthening the information architecture for climate-related risk disclosure by banks and corporates. SECP's IFRS S2 mandate is a direct response to these structural reform requirements. For Pakistani CFOs and boards, this connection matters: ESG compliance is not an isolated regulatory requirement. It is linked to the conditions governing Pakistan's access to concessional international financing.

A company that helps its regulator demonstrate credible, investor-grade climate disclosure is contributing to conditions that stabilise the country's external financing. One that ignores SECP IFRS S2 requirements creates reputational risk for the broader market's credibility with institutional lenders.

For the full analysis of the IMF RSF facility and its climate disclosure conditionality for Pakistan, read Pakistan's IMF Climate Facility and What It Means for Corporate ESG Reporting.

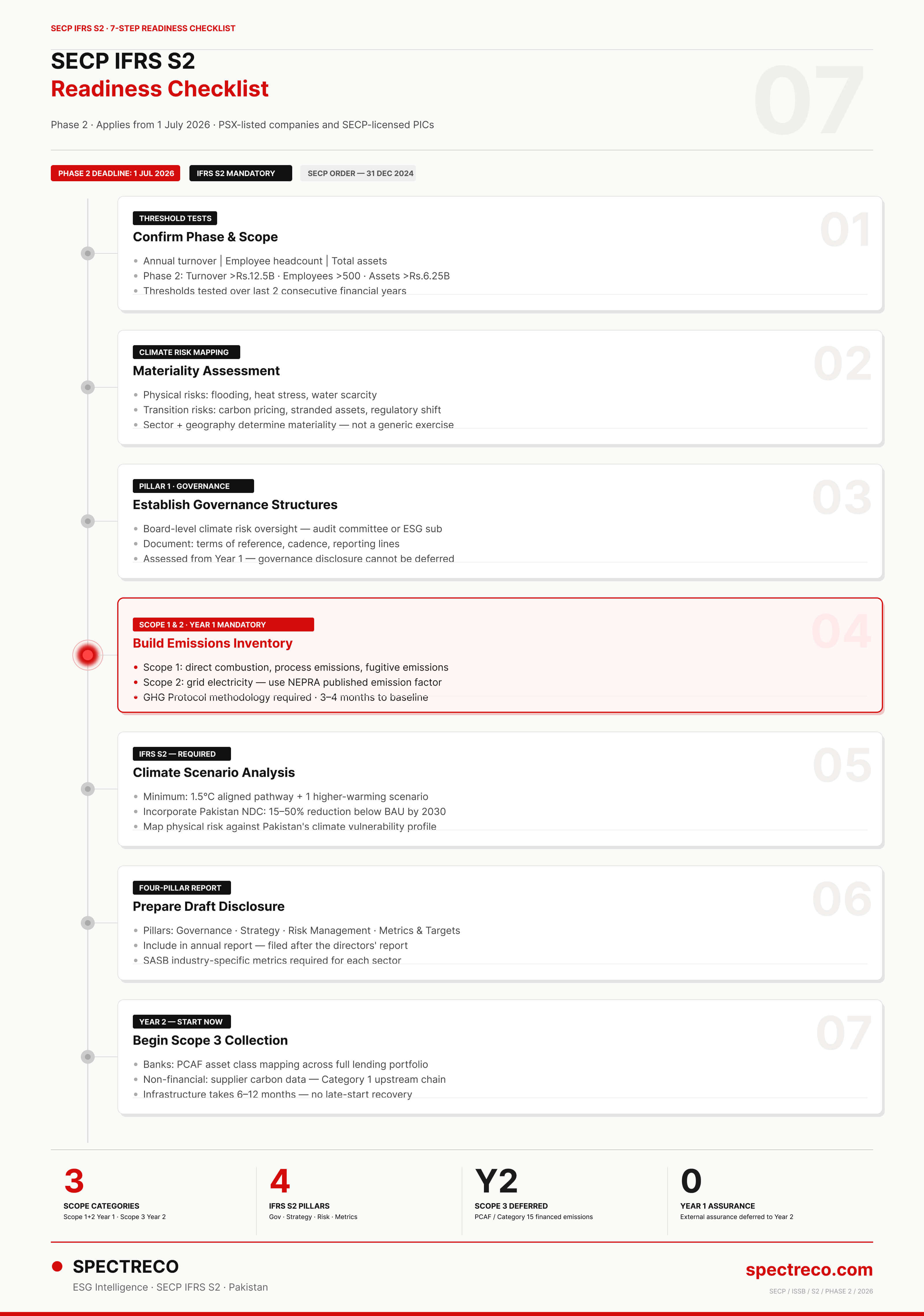

7-Step SECP IFRS S2 Readiness Checklist

The following seven steps reflect the sequence Spectreco recommends for Phase 2 companies beginning their compliance programme now. The steps assume a company with no prior IFRS S2 reporting history.

Step 1: Confirm Your Phase and Scope

Run the three threshold tests against your company's last two consecutive financial years: annual turnover, employee headcount, and total assets. Confirm whether you fall into Phase 1 (already begun), Phase 2 (July 1, 2026), or Phase 3 (July 1, 2027). The exact thresholds are set out in the SECP Order under Section 238, Companies Act 2017. Get legal confirmation of your PIC status if you are a non-listed SECP-licensed entity.

Step 2: Conduct a Materiality Assessment

Under IFRS S2, you must identify which climate-related risks and opportunities are material to your business model. This means mapping physical risks (flooding, heat, water stress) and transition risks (carbon pricing, stranded assets, regulatory change) to your operations, supply chain, and revenue streams. Sector and geography determine materiality. A textile manufacturer in Punjab faces different risk concentrations than a cement company in Khyber Pakhtunkhwa.

Step 3: Establish Governance Structures

Assign board-level oversight of climate risk. This typically sits with the audit committee or a named ESG subcommittee. Document the terms of reference, meeting cadence, and reporting lines. Governance is Pillar 1 of IFRS S2 and is assessed from Year 1. A board that cannot demonstrate formal climate oversight will fail the first assurance review.

Step 4: Build Your Emissions Inventory (Scope 1 and 2 First)

Start data collection for Scope 1 (direct combustion, process emissions, fugitive emissions) and Scope 2 (grid electricity, purchased heat). Use the GHG Protocol methodology and NEPRA's published grid emission factor for Scope 2 calculations. For most non-financial listed companies, Scope 1 and 2 can be baselined within three to four months with a structured data collection programme across operational sites.

Step 5: Run Climate Scenario Analysis

IFRS S2 requires scenario analysis covering at least one scenario aligned with limiting warming to 1.5 degrees Celsius and at least one higher-warming scenario. For Pakistani companies, scenarios should incorporate Pakistan's Nationally Determined Contribution (NDC), which sets a 15 to 50 percent emissions reduction target below business-as-usual by 2030, and the physical risk implications of the country's climate vulnerability profile.

Step 6: Prepare Your Draft Disclosure

Draft the four-pillar disclosure against the IFRS S2 requirements using the structure above. The sustainability report must be included in your annual report, after the directors' report. Ensure all quantitative figures use the GHG Protocol methodology and that SASB industry-specific metrics for your sector are incorporated. First-year assurance is not yet mandatory, but preparing assurance-ready documentation from Year 1 saves significant time in Year 2.

Step 7: Begin Scope 3 Data Collection in Parallel

Even though Scope 3 disclosure is deferred to Year 2, the data collection infrastructure takes time to build. For financial institutions, this means starting PCAF asset class mapping now. For non-financial companies, it means working with key suppliers on carbon footprint data. Starting Year 2 preparation before Year 1 reporting is complete is the difference between a managed transition and a compliance emergency. Spectreco's SECP IFRS S2 platform supports both Scope 3 mapping and PCAF implementation for Pakistani companies.

Top Consultants for SECP Compliance in Pakistan

With Phase 2 beginning on July 1, 2026, and Phase 1 already under way, PSX-listed companies need advisory capacity that understands both the IFRS S2 standard and the Pakistani regulatory environment. Below are three firms actively supporting SECP IFRS S1 and S2 compliance programmes in Pakistan.

1. Spectreco

Spectreco is a sustainability technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore. The Lahore office works directly with PSX-listed companies across all three phases of the SECP mandate, combining platform-based compliance infrastructure with advisory services built for Pakistan's specific regulatory requirements.

What separates Spectreco from audit-house advisory is the combination of purpose-built ESG software and on-the-ground Pakistan presence. Most SECP-listed companies are not just missing a consultant. They are missing a data system that can manage Scope 1 and 2 emissions, handle PCAF financed emissions calculations for their loan portfolios, run climate scenario analysis against Pakistan's physical risk profile, and generate four-pillar IFRS S2 disclosure outputs from a single platform. Spectreco provides all of this as an integrated product, not a series of disconnected consulting engagements.

Spectreco's compliance work spans three areas that matter most for Phase 2 companies right now:

- GHG inventory and PCAF financed emissions: Scope 1, 2, and Scope 3 Category 15 measurement using GHG Protocol methodology and NEPRA grid emission factors for Pakistan. PCAF asset-class mapping for banks and NBFCs using the PCAF Global GHG Accounting Standard v3.

- Four-pillar IFRS S2 report preparation: Governance, strategy, risk management, and metrics and targets disclosures drafted to SECP requirements, with SASB industry-specific metrics incorporated for sectors including textiles, cement, fertilisers, and financial services.

- Assurance-ready documentation from Year 1: Because mandatory auditor assurance begins in Year 2, companies that build audit-ready data infrastructure in Year 1 avoid the cost and delay of rebuilding it under assurance pressure later.

Spectreco also launched the world's first Shariah-compliant ESG Index in partnership with AlBaraka Forum in April 2025, which reflects deep familiarity with Pakistan's capital market and Islamic finance context.

Relevant pages for Phase 2 companies:

- AI-Native ESG Platform — SECP IFRS S2 compliance workflows, Scope 1/2/3, PCAF financed emissions

- Compliance, Reporting and Disclosures Advisory — first-year report preparation, gap assessment, audit-ready documentation

- Virtual Sustainability Office (VSO) — embedded ESG capacity for companies without in-house sustainability teams

- Capacity Building and Training — board and leadership climate governance training for IFRS S2 Pillar 1

- ESG Maturity Rating — diagnostic baseline for companies starting their SECP compliance programme

Source: Spectreco, SECP IFRS S2 Platform; Spectreco AlBaraka Forum Shariah-Compliant ESG Index, April 2025

2. KPMG Taseer Hadi and Co.

KPMG Taseer Hadi and Co. is Pakistan's KPMG member firm and one of the longest-established professional services firms in the country, with offices in Karachi, Lahore, and Islamabad. It was a founding member of the ESG Task Force convened by the Pakistan Stock Exchange (PSX), SECP, and the Pakistan Institute of Corporate Governance (PICG) that developed the original ESG Disclosure Guidelines for PSX-listed companies. That early involvement in shaping Pakistan's ESG regulatory architecture gives KPMG institutional knowledge of where the SECP framework came from and how the regulator expects it to be applied.

KPMG Pakistan's ESG practice covers three areas directly relevant to SECP IFRS S2 compliance. Its ESG assurance service provides formal opinions over reported ESG metrics and disclosures delivered under ISAE 3000, at both limited and reasonable assurance levels. This is the assurance standard that will apply when mandatory auditor assurance begins in Year 2 of SECP compliance. Its climate risk and decarbonisation strategy service helps companies build the scenario analysis and risk management disclosures required under IFRS S2 Pillars 2 and 3. Its sustainability supply chain service addresses Scope 3 Category 1 (purchased goods and services) for non-financial companies that need upstream emissions data.

KPMG Pakistan also publishes a quarterly Accounting and Sustainability Reporting Newsletter covering SECP regulatory updates, amendments to IFRS S2, and GHG Protocol guidance, which functions as a practical resource for company secretaries and CFOs managing the compliance timeline.

Where KPMG adds most value for SECP compliance is in assurance credibility. If your institution needs Year 2 assurance signed by an auditor that institutional investors and the SECP will recognise, KPMG's audit relationships and ISAE 3000 delivery capability are a practical consideration. Its limitation is the same as all Big 4 firms: advisory engagements are typically scoped per project, without the integrated platform infrastructure that automates ongoing data collection, emissions calculation, and reporting.

3. EY Ford Rhodes

EY Ford Rhodes is the EY member firm in Pakistan, with offices in Karachi, Lahore, and Islamabad. It is part of EY's global Climate Change and Sustainability Services (CCaSS) practice, which Verdantix named in its 2026 Green Quadrant as one of five firms with comprehensive end-to-end ESG capabilities globally. EY's climate and sustainability service line uses its AI platform EY.ai and the EY Nexus ecosystem to support emissions measurement, regulatory reporting, and sustainability disclosure for listed companies.

For Pakistani listed companies, EY Ford Rhodes is relevant in two specific situations. First, for companies that already use EY as their statutory auditor: having the advisory and assurance work handled within the same global firm reduces coordination risk and can shorten the Year 2 assurance timeline. Second, for companies with overseas operations or international institutional investors requiring disclosures under CSRD, TCFD, or SEC climate rules simultaneously with SECP IFRS S2: EY's global reach means one advisory team can manage multi-jurisdiction reporting without the complexity of coordinating across separate firms.

EY Ford Rhodes's Pakistan-specific ESG practice is less publicly documented than KPMG Taseer Hadi's, which has published more Pakistan-specific SECP guidance. Both firms require engagement-by-engagement scoping and neither offers a continuously updated compliance platform in the way Spectreco does. For Phase 2 companies that need both ongoing data infrastructure and one-off assurance, a combined approach using Spectreco's platform with KPMG or EY for Year 2 auditor assurance is a practical structure that several Pakistan-based financial institutions are already using.

Source: EY Global CCaSS; Verdantix 2026 Green Quadrant ESG Consulting; EY Pakistan Office Locations

Frequently Asked Questions (FAQs)

The following questions represent the most common queries from CFOs, company secretaries, and sustainability teams at PSX-listed companies preparing for SECP IFRS S2 compliance.

How Spectreco Supports SECP IFRS S2 Compliance

Spectreco is an ESG technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore. From the Lahore office, Spectreco works directly with PSX-listed companies navigating the SECP IFRS S2 mandate across all three phases. Visit the Spectreco ESG Reporting Advisory page for details on how the advisory practice supports Phase 2 readiness.

The Spectreco SECP IFRS S2 platform manages the full compliance workflow: materiality assessment, Scope 1 and 2 emissions inventory, climate scenario analysis, PCAF-methodology financed emissions calculation for financial institutions, four-pillar IFRS S2 report generation, and audit-ready documentation. This is Spectreco's competitive view of its platform capabilities for SECP compliance.

Phase 2 begins July 1, 2026. If your company has not yet begun its readiness programme, the window for a structured build is closing.

Book a SECP IFRS S2 readiness call with the Spectreco Pakistan team at spectreco.com demo. Bring your last two years of financial data and your investor relations calendar.

More From Our Blog

Your ESG Journey?