Singapore Climate Disclosure: SGX & ACRA ISSB Timeline

Singapore Mandatory Climate Reporting: The SGX and ACRA ISSB Timeline for 2026 and Beyond

Singapore has become Southeast Asia’s clearest test case for mandatory climate disclosure. From financial years starting on or after 1 January 2025, every company listed on the Singapore Exchange must report Scope 1 and Scope 2 greenhouse gas (GHG) emissions. Scope 1 covers direct emissions from sources a company owns or controls. Scope 2 covers indirect emissions from purchased electricity, heat, or cooling.

That baseline did not move when regulators eased other deadlines in August 2025. Singapore mandatory climate reporting under SGX RegCo and ACRA now runs on a staged, ISSB-based timeline that stretches from FY2025 to FY2032, and it reaches past listed issuers to large private companies.

Spectreco, a global sustainability technology and advisory firm with offices in Atlanta, Lahore, Lisbon, Dubai, and Muscat, tracks these regimes across markets. This guide sets out who reports what, by when, and what the extended timelines mean for finance and sustainability teams building climate data systems in the region. The disclosure standards come from the International Sustainability Standards Board (ISSB), which issued IFRS S1 and IFRS S2 in June 2023.

Source: IFRS Foundation, IFRS S2 Climate-related Disclosures

Is Climate Reporting Mandatory in Singapore?

Yes. All companies listed on the Singapore Exchange (SGX) must report Scope 1 and Scope 2 emissions from FY2025. Broader ISSB-based climate disclosures phase in by company size through FY2030. Large non-listed companies join from FY2030. Two regulators set the regime: SGX RegCo and ACRA.

Singapore Exchange Regulation (SGX RegCo) governs listed issuers through the SGX Listing Rules, specifically Rules 711A and 711B. The Accounting and Corporate Regulatory Authority (ACRA) covers large non-listed companies and is developing local sustainability disclosure standards based on the ISSB standards. Rather than adopting IFRS S1 and IFRS S2 wholesale, Singapore took a climate-first, ISSB-informed route: it embedded the IFRS S2 climate requirements into the listing rules first, then phased the rest.

Source: ACRA, Sustainability reporting overview; Persefoni, ISSB-aligned reporting in Singapore

The SGX Listed-Company Timeline: A Three-Tier Structure

Scope 1 and 2 reporting is the common floor: every SGX-listed issuer, including overseas-incorporated companies, business trusts, and real estate investment trusts, reports these from FY2025. On top of that floor sits a three-tier structure for the other ISSB-based climate-related disclosures (CRD): governance, strategy, risk management, and metrics and targets.

Source: ACRA & SGX RegCo, Extended timelines for most climate reporting requirements, 25 August 2025; Linklaters, Singapore extended timelines

Straits Times Index constituents lead from FY2025

The 30 Straits Times Index (STI) constituents, the largest SGX companies by market capitalisation, carry the earliest and fullest obligations. They report other ISSB-based CRD from FY2025 and Scope 3 emissions from FY2026. Scope 3 covers value-chain emissions, which for many groups dwarf their own operational footprint. STI status is fixed as at 30 June 2025, so a company that later leaves the index still reports.

Source: ACRA news announcement, footnotes 2 and 3

Non-STI issuers with S$1 billion or more in market cap: FY2028

Non-STI listed companies with a market capitalisation of S$1 billion and above must report other ISSB-based CRD from FY2028. The market-cap test is applied at the close of market on 30 June 2025, or on the listing date for companies that listed later. Once a company crosses the threshold, the obligation sticks even if its market cap subsequently falls below S$1 billion.

Source: ACRA news announcement, footnote 4

Non-STI issuers below S$1 billion: FY2030

Smaller non-STI issuers, those below the S$1 billion mark, report other ISSB-based CRD from FY2030. That is a five-year runway from the Scope 1 and 2 start date, and the group ACRA and SGX RegCo singled out as needing the most time to build data collection and governance.

Source: Allen & Gledhill, ACRA and SGX RegCo extend timelines

What the August 2025 Extension Actually Changed

On 25 August 2025, ACRA and SGX RegCo extended most climate reporting timelines. They cited the uncertain global economic climate and feedback from the Singapore Business Federation that smaller listed companies needed more time to be ready for ISSB-based CRD. SGX RegCo Chief Executive Tan Boon Gin framed it as a more targeted, proportionate approach in which the largest companies lead.

The important point for planning is what did not change. Scope 1 and 2 disclosure stayed mandatory from FY2025 for all listed companies, because that data is more circumscribed and tracks decarbonisation progress. STI obligations, including Scope 3 from FY2026, also held firm. What moved was the timing for everyone else.

- Non-STI CRD deadlines were pushed to FY2028 and FY2030 by market cap.

- External limited assurance over Scope 1 and 2 was deferred to FY2029 for all listed companies.

- Large non-listed company reporting slipped from FY2027 to FY2030, and their assurance from FY2029 to FY2032.

Source: ACRA & SGX RegCo joint media release, 25 August 2025; ESG Today, Singapore delays climate reporting requirements

Do Large Non-Listed Singapore Companies Have to Report?

Yes. Large non-listed companies, defined by ACRA as those with at least S$1 billion in annual revenue and at least S$500 million in total assets, must report ISSB-based climate disclosures, including Scope 1 and 2, from FY2030. Scope 3 stays voluntary until further notice. Limited assurance over Scope 1 and 2 follows in FY2032.

The detailed obligations for these large non-listed companies are expected to be written into Singapore’s Companies Act 1967, with ACRA set to launch a public consultation on the amending bill. A useful exemption exists: a large non-listed company can be exempt where its parent already reports climate disclosures using ISSB-aligned local standards or equivalent standards, for example the European Sustainability Reporting Standards (ESRS) under the EU’s Corporate Sustainability Reporting Directive (CSRD), provided the subsidiary’s activities appear in a publicly available consolidated report.

ACRA has also signalled it will review whether to extend mandatory reporting to smaller non-listed companies, those with revenue from S$100 million to below S$1 billion. No date is fixed for that group yet.

Source: Linklaters, ESG Quick Guide: Singapore mandatory climate reporting regime; ACRA, requirements and timeline

When Is Assurance Required in Singapore?

External limited assurance over Scope 1 and 2 emissions is required from FY2029 for all listed companies and from FY2032 for large non-listed companies. Assurance must come from a registered climate auditor: an ACRA-registered audit firm, or a testing, inspection, and certification firm accredited by the Singapore Accreditation Council.

Limited assurance means an independent reviewer expresses moderate confidence that the emissions data is not materially misstated. It is a lighter standard than the reasonable assurance applied to audited financial statements, but it still forces disciplined measurement, documentation, and traceable data lineage well before the assurance year arrives.

Source: Persefoni, ISSB-aligned reporting in Singapore; Linklaters, ESG Quick Guide

What Singapore’s Timeline Means for Companies Across Southeast Asia

Singapore is the ISSB frontrunner of ASEAN, and its regime sits inside a wider national push. The Singapore Green Plan 2030 anchors a net-zero-by-2050 target, and the carbon tax rises from S$25 to S$45 per tonne in 2026. Climate data is moving from a marketing exercise to priced, assured, regulated information.

Source: Slaughter and May, ESG in APAC 2025: Singapore

The extension bought time, not a reprieve. The hardest parts of ISSB reporting, a defensible Scope 3 inventory and assurance-grade controls, still land. Companies that treat FY2028 or FY2030 as distant tend to discover in year one that their emissions data was never built to survive an assurance review.

Cross-border groups face the sharpest version of this. A company listed in Singapore with Australian operations also has to reckon with AASB S2, Australia’s mandatory climate standard, while a European footprint pulls in CSRD and the ESRS. Managing three ISSB-derived regimes from one data set is the real design problem.

Enforcement is not theoretical either. For listed issuers, failure to meet SGX disclosure obligations can trigger regulatory action from SGX RegCo, and greenwashing remains a stated supervisory priority in Singapore. Even where no penalty lands, weak or late disclosure erodes investor confidence and can lift the cost of capital, which is the exact outcome most boards are trying to prevent.

Source: Slaughter and May, ESG in APAC 2025: Singapore

This is where Spectreco positions its work. The cloud-native Spectreco platform maps ESG data once and reuses it across ISSB, CSRD/ESRS, and local listing rules, with audit-ready outputs and transparent data lineage. On the advisory side, Spectreco’s compliance, reporting, and disclosures team designs the reporting architecture, gap-maps current practice against SGX and ISSB requirements, and prepares companies for external assurance.

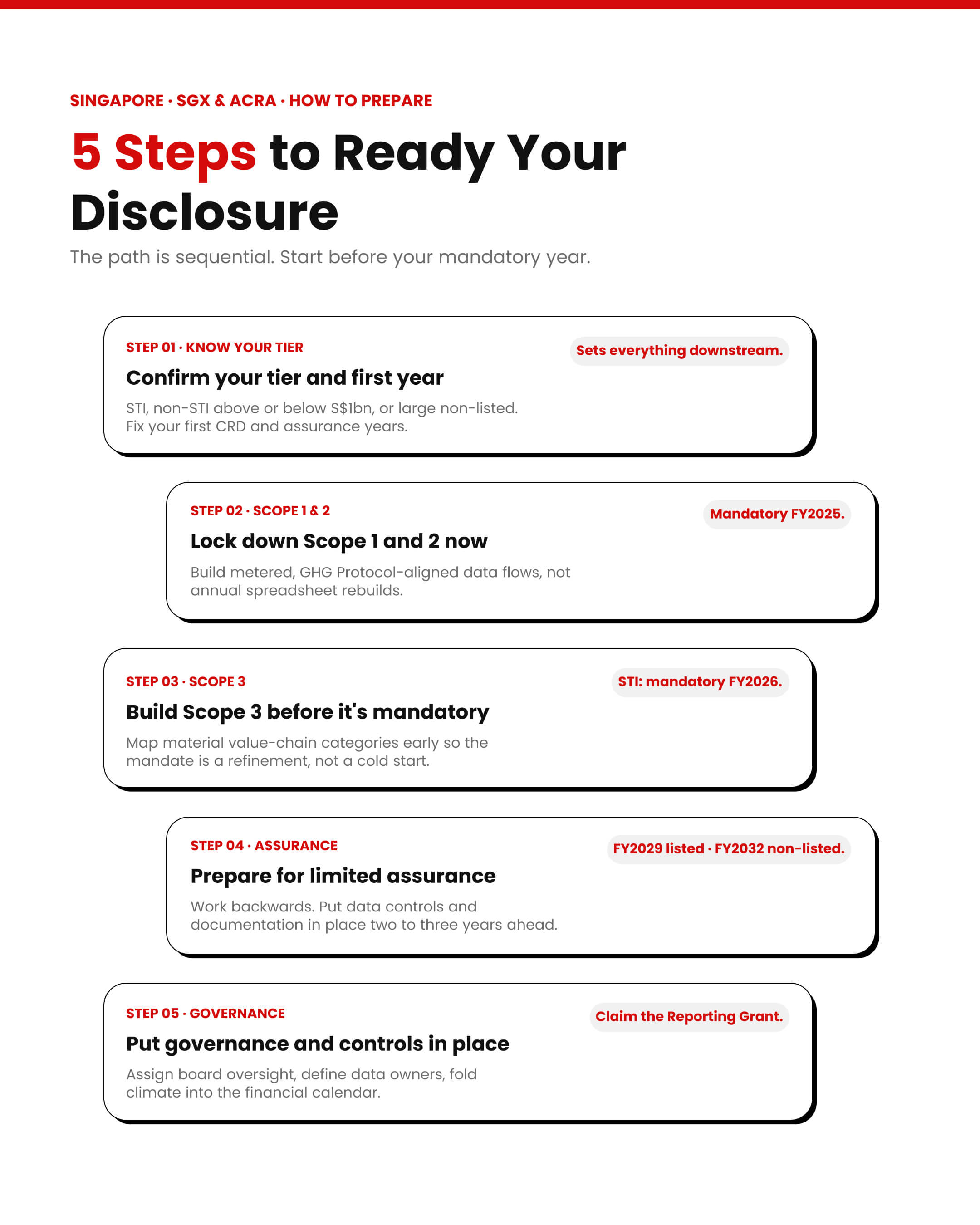

How to Prepare for Singapore’s Climate Disclosure Deadlines

The path to compliance is sequential. These five steps map to the phased timeline and are worth starting before your mandatory year.

- Confirm your tier and first reporting year. Establish whether you are an STI constituent, a non-STI issuer above or below S$1 billion, or a large non-listed company, then fix your first mandatory CRD and assurance years.

- Lock down Scope 1 and 2 data now. This is already mandatory for listed issuers. Build metered, GHG Protocol-aligned data flows rather than annual spreadsheet reconstructions.

- Build a Scope 3 inventory before it is mandatory. Even where Scope 3 is voluntary, map material value-chain categories early so the eventual mandate is a refinement, not a cold start.

- Prepare for limited assurance. Work backwards from your assurance year (FY2029 for listed, FY2032 for large non-listed) and put data controls and documentation in place two to three years ahead.

- Put governance and controls in place. Assign board oversight, define data owners, and integrate climate reporting into the financial reporting calendar. Apply for the Sustainability Reporting Grant to offset preparation costs.

Source: ACRA, sustainability reporting requirements and timeline

Frequently Asked Questions (FAQs)

Plan Your Singapore Disclosure Timeline With Spectreco

Map your SGX or ACRA reporting year, then build the data systems and assurance readiness to meet it. Book a Singapore climate disclosure readiness assessment with Spectreco’s compliance, reporting, and disclosures team, or explore more regional analysis in the Spectreco ESG Intelligence hub.

More From Our Blog

Your ESG Journey?