AASB S2, TCFD & CSRD: Australian Global Operations

AASB S2, TCFD, and CSRD: What Australian Companies with Global Operations Must Know

An Australian company with a London office and a German subsidiary now answers to three climate reporting regimes at once: AASB S2 in Canberra, the remains of the TCFD now living inside the global ISSB baseline, and the European Union's CSRD in Brussels. For Australian companies with global operations, the multi-framework question stopped being theoretical the moment AASB S2 became law. Which standard governs which entity, and where do the obligations overlap, diverge, or contradict?

Spectreco, a sustainability technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore, works with chief financial officers (CFOs) and chief sustainability officers (CSOs) untangling exactly this. The short version: the three frameworks share a spine, but they split on the one question that changes everything, which is what you are required to treat as material.

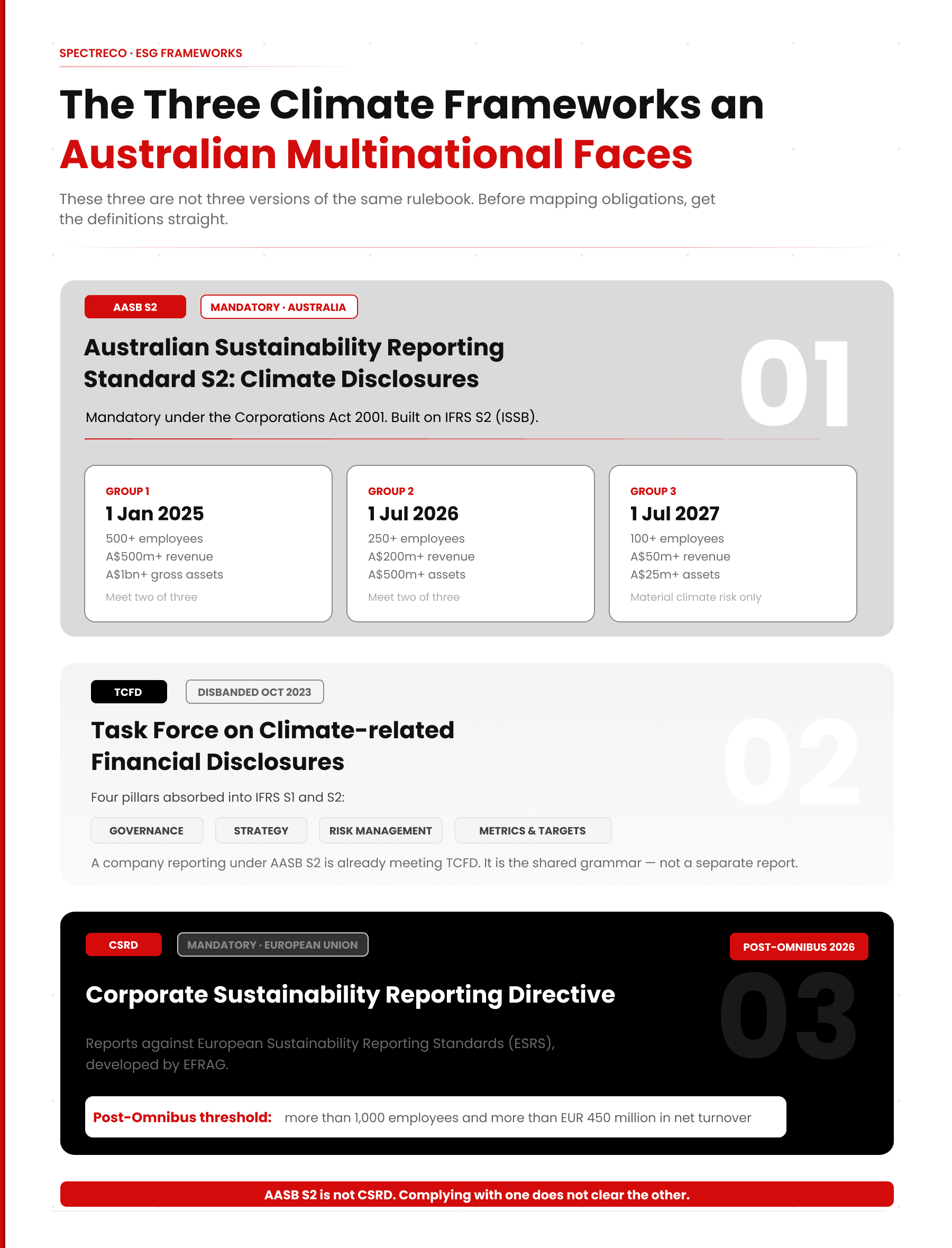

The three climate frameworks an Australian multinational faces

Before mapping obligations, get the definitions straight. These three are not three versions of the same rulebook.

AASB S2: the Australian standard

AASB S2 (Australian Sustainability Reporting Standard S2: Climate-related Disclosures) is mandatory under the Corporations Act 2001 and built on IFRS S2, the climate standard issued by the International Sustainability Standards Board (ISSB). It phases in by company size:

- Group 1: financial years from 1 January 2025. Two of: more than 500 employees, A$500m+ consolidated revenue, A$1bn+ gross assets.

- Group 2: from 1 July 2026. Two of: more than 250 employees, A$200m+ revenue, A$500m+ assets. Asset owners with A$5bn+ under management are also captured.

- Group 3: from 1 July 2027. More than 100 employees, A$50m+ revenue, A$25m+ assets, and only where material climate risk exists.

Source: Australian Accounting Standards Board / Treasury Laws Amendment Act 2024, via PwC Australia

TCFD: the framework that no longer files on its own

The Task Force on Climate-related Financial Disclosures (TCFD), created by the Financial Stability Board in 2015, was disbanded in October 2023. Its four pillars (governance, strategy, risk management, and metrics and targets) were absorbed into IFRS S1 and S2, and the IFRS Foundation took over monitoring from 2024.

A company reporting under AASB S2 is, in practice, already meeting TCFD. Treat TCFD as the shared grammar all three regimes speak, not a separate report to produce.

Source: IFRS Foundation

CSRD / ESRS: the European regime

CSRD (Corporate Sustainability Reporting Directive) is the EU's mandatory sustainability reporting law. In-scope companies report against the European Sustainability Reporting Standards (ESRS), developed by EFRAG. After the Omnibus I simplification package, approved by the European Parliament in December 2025 and adopted by the Council in February 2026, CSRD applies to EU entities with more than 1,000 employees and more than EUR 450 million in net turnover.

Source: Accountancy Europe, Omnibus explained

Spectreco has written separately on why the cuts did not let European reporters off the hook: see The EU Omnibus Trap: ESG Reporting Is Not Optional.

What is double materiality, and does it apply in Australia?

Double materiality is the CSRD requirement to report both how climate affects your business and how your business affects climate and society. AASB S2 uses financial materiality only. It asks how climate affects the company, not the reverse. So double materiality does not apply to Australian reporting under AASB S2.

Financial materiality, used by AASB S2 and IFRS S2, asks you to disclose climate risks and opportunities that could reasonably affect your cash flows, access to finance, or cost of capital. It is an outside-in view: the world acting on the company.

Double materiality, used by CSRD and ESRS, keeps that financial lens and adds impact materiality: the company's own effect on people and the environment. It runs both directions, outside-in and inside-out.

This single difference is why "we already comply with AASB S2" does not clear a CSRD obligation. Your EU entity still has to assess and report its impacts, not just its climate risk exposure.

AASB S2 vs CSRD (ESRS) vs TCFD: the comparison that matters

Set side by side, the differences in materiality, scope, and assurance are what decide your workload.

If your Australian company also has EU operations, here is what you need

Map the obligation to the entity, not to the group. The framework follows where the company is incorporated and how big it is.

- If you are Group 1 or Group 2 in Australia, you are already producing (or soon will) an AASB S2 climate statement with limited assurance over Scope 1, Scope 2, and governance.

- If you have an EU subsidiary above 1,000 employees and EUR 450m turnover, that entity reports under CSRD with double materiality, covering far more than climate.

- If your EU presence sits below those thresholds, you may be out of CSRD scope entirely after Omnibus. Confirm against the final thresholds before building anything.

- Non-EU parent groups that meet the EU thresholds begin reporting under CSRD in 2029 on fiscal year 2028 data. Plan for it now if your EU turnover is large.

Source: BDO, CSRD Post-Omnibus Revised Scope

How to run one reporting system for AASB S2 and CSRD

The frameworks overlap enough that building two parallel programmes is wasted money. Build one climate core, then add the European layer.

- Map your legal entities to frameworks. List every reporting entity and tag it AASB S2, CSRD, or both. Most groups find the two obligations sit on different entities.

- Build the climate core once. IFRS S2 and ESRS E1 are highly aligned, confirmed by the joint interoperability guidance from the IFRS Foundation and EFRAG. Collect governance, strategy, scenario analysis, and Scope 1, 2 and 3 emissions data to the stricter of the two standards (Scope 1 and 2 are direct and purchased-energy emissions; Scope 3 is value-chain emissions).

Source: IFRS Foundation and EFRAG, Interoperability Guidance (May 2024)

- Add the EU-only layer. For CSRD entities, run a double materiality assessment and extend reporting to the impact topics ESRS requires that AASB S2 never asks for.

- Assure to the highest bar. Australia needs limited assurance now and reasonable assurance by financial years starting on or after 1 July 2030. Build evidence trails that survive an external auditor from day one.

- Govern it in one place, not six spreadsheets. A single ESG data platform keeps the same emissions figure flowing into both the Australian climate statement and the European report, so the two never contradict each other under assurance.

Get this wrong and the cost is not only rework. Under AASB S2, directors face civil penalties for false or misleading climate statements, with per-offence figures running from A$93,900 to A$751,200, and poor disclosure quality feeds straight into a higher cost of capital.

Source: Corrs Chambers Westgarth analysis of the Corporations Act 2001

Frequently asked questions (FAQs)

Close the gaps before an auditor finds them

If your group reports in Australia and Europe, the risk is not missing one framework. It is reporting the same emissions figure two different ways and failing assurance on both. Spectreco runs a multi-jurisdiction ESG compliance gap assessment that maps every entity to its framework, flags the AASB S2 and CSRD requirements you are missing, and shows where one data set can serve both.

Book your gap assessment with Spectreco and walk into your next reporting cycle knowing exactly which standard governs which entity.

.jpg)

.jpg)

More From Our Blog

Your ESG Journey?