Pakistan Textiles & EU CBAM: Carbon Data Before 2027.

Pakistan Textile Exporters and EU CBAM: The Carbon Data You Need Before 2027

A Pakistan Stock Exchange (PSX) listed textile exporter shipping bed linen to Germany is now being asked for the same thing from three different directions: verified carbon data. The Pakistan textile exporters EU CBAM ESG carbon data 2027 question is not really about a tariff that lands next quarter. It is about the emissions dataset European market access will demand before 2027, and whether your firm can produce it on request.

Here is the fact most vendors get wrong. The EU Carbon Border Adjustment Mechanism (CBAM), the bloc's carbon tariff on imports, does not tax textiles today. It covers six heavy industries, and fabric is not one of them. What is coming for textiles is the EU Digital Product Passport, and it starts arriving from February 2027. The useful news for Pakistani exporters: the carbon data all of this needs is largely the data the Securities and Exchange Commission of Pakistan (SECP) already makes you collect.

In this article

- Does EU CBAM apply to Pakistani textiles today?

- Why Pakistani textile exporters are exposed

- The EU Digital Product Passport: the obligation that bites first

- How SECP IFRS S2 carbon data feeds CBAM and the DPP

- A 5-step carbon-data readiness plan

- FAQ

What Is EU CBAM, and Does It Apply to Pakistani Textiles Today?

No. As of its definitive phase on 1 January 2026, CBAM applies only to imports of iron and steel, aluminium, cement, fertilisers, hydrogen, and electricity. Textiles and apparel sit outside its scope and carry no direct CBAM cost today. The exposure for Pakistani textile firms is real, but it arrives through different routes.

CBAM works by attaching a carbon price to covered imports that mirrors the cost EU manufacturers pay under the EU Emissions Trading System (ETS). Importers buy CBAM certificates, each equal to one tonne of embedded carbon dioxide equivalent, priced to the ETS. The aim is to stop carbon leakage, where production shifts to countries with weaker carbon rules. Fabric and finished garments are not on the covered list.

Sources: European Commission, CBAM sectors

The route textiles actually take into CBAM

CBAM is built to expand, so the question for exporters is timing, not whether. Two moves matter.

- Downstream expansion from 2028. In December 2025 the Commission proposed adding roughly 180 steel and aluminium-intensive downstream products, such as vehicle parts and appliances, agreed by member states in June 2026. Textiles are not in this batch.

- Chemicals and polymers by around 2030. The EU intends to widen CBAM to all sectors covered by the ETS, which eventually reaches the chemical feedstocks behind synthetic fibres: polyester, nylon, acrylic, elastane. Once polymers are in scope, each kilogram of synthetic fibre could need a verified carbon declaration, with conservative default values applied where primary supplier data is missing.

Sources: Akin Gump, CBAM downstream scope expansion | Climate Leadership Council, EU CBAM guide

The practical read: a cotton-heavy exporter has a longer runway on CBAM itself. A synthetic or blended-fabric exporter should track the polymer timeline closely, because default emissions values tend to reflect the highest intensity observed in a producer country, and they are expensive.

Why Pakistani Textile Exporters Are Exposed

Exposure here is structural, not incidental. Textiles account for close to 60 percent of Pakistan's total exports. In 2024, textiles made up 75.8 percent of Pakistan's total exports to the EU, and the EU took 27.6 percent of Pakistan's total exports that year. Pakistan is the single largest beneficiary of the EU's Generalised Scheme of Preferences Plus (GSP+), which grants duty reductions in exchange for implementing 27 international conventions, including on environmental protection.

Sources: CDPR, Pakistan textiles under CBAM | Pakistan Business Council, trade with the EU | European Commission, EU-Pakistan trade

Put those numbers together and the risk is clear. A large, EU-concentrated export base means even a moderate compliance cost lands on a lot of shipments, and GSP+ ties that access to environmental performance. The direction of travel is one way.

The buyer pressure is already here, ahead of any tariff. European customers now ask Pakistani suppliers for Scope 1 and Scope 2 emissions data as a condition of doing business, which is why the climate report is becoming a commercial document long before a regulator audits it. Spectreco covers the mandate driving that shift in its SECP Phase 2 and IFRS S2 readiness guide.

The EU Digital Product Passport: The Obligation That Bites First

The nearer-term pressure is not CBAM. It is the EU Digital Product Passport (DPP), a core tool of the Ecodesign for Sustainable Products Regulation (ESPR, Regulation (EU) 2024/1781). The Commission's April 2025 working plan named textiles the top-priority product group, with the DPP rolling out gradually from February 2027.

Sources: Pakistan & Gulf Economist, Pakistan's textile exports and the EU's DPP

In practice, the DPP means a product entering the EU market must carry a verifiable digital record of its production history and sustainability credentials. For a textile exporter, that record has to demonstrate traceability across origin, production stages, material composition, and environmental performance, including carbon footprint, before goods can move through European supply chains.

Why this is harder than a report

A sustainability report is written once a year at the entity level. The DPP is per product. You need to attribute emissions and material data down to the individual item, and pull verified data up from your yarn and fabric suppliers. This is the same product-level demand CBAM will eventually make for synthetic fibre, which is why the two obligations reward the same groundwork.

How SECP IFRS S2 Carbon Data Feeds CBAM and the DPP

The Securities and Exchange Commission of Pakistan (SECP) mandated IFRS S1 and IFRS S2, the ISSB's Climate-related Disclosures standard issued in June 2023, by order dated 31 December 2024. Reporting is phased: Phase 1 from 1 July 2025, Phase 2 from 1 July 2026, and Phase 3 from 1 July 2027. Textile exporters that meet two of three size thresholds sit squarely in Phase 2, with auditor assurance beginning in the second year.

Sources: IFRS Foundation, Jurisdictional Profile: Pakistan | SECP notification (via ProPakistani)

IFRS S2 follows four pillars: governance, strategy, risk management, and metrics and targets. The metrics pillar is the one that matters here. It requires Scope 1 (direct emissions from owned sources), Scope 2 (purchased electricity, heat, steam or cooling), and material Scope 3 (value-chain) emissions, all measured under the Greenhouse Gas (GHG) Protocol.

That GHG Protocol inventory is the shared spine. The table below shows how the same emissions data serves three regimes, and where each one asks for more.

Shared foundation: a GHG Protocol Scope 1 and 2 inventory measured at facility level.

The overlap is the opportunity. Build the GHG Protocol inventory once for SECP and you hold the backbone for CBAM and the DPP. The gap is granularity. SECP lets you report at entity level, while CBAM and the DPP need the same emissions attributed to a product and a facility, plus supplier traceability the DPP checks. Treat SECP IFRS S2 as the foundation, not the finish line. The value-chain data it starts you on is the same data that feeds a CSRD double materiality assessment for buyers who report under the EU's Corporate Sustainability Reporting Directive (CSRD).

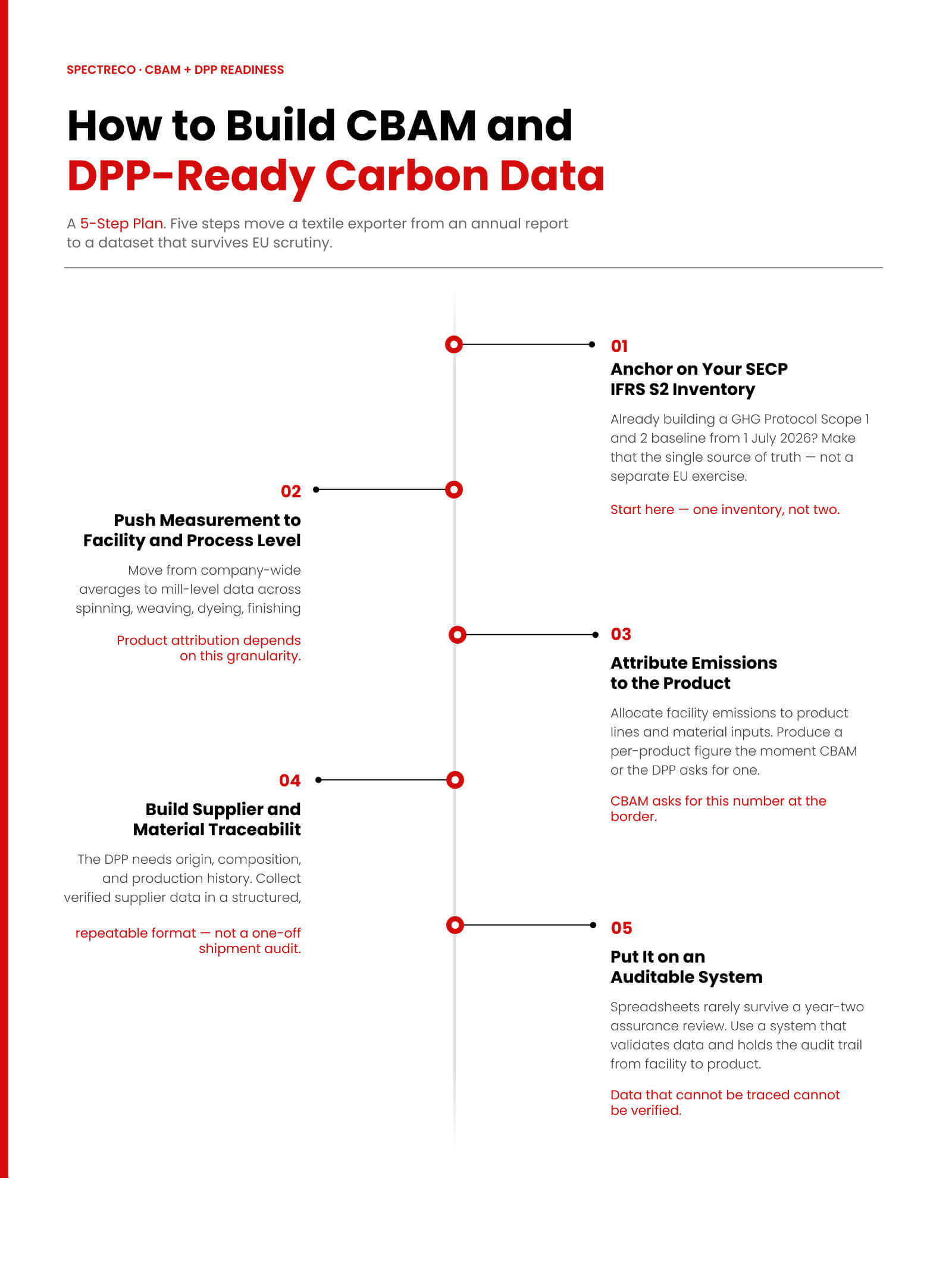

How to Build CBAM and DPP-Ready Carbon Data: A 5-Step Plan

Five steps move a textile exporter from an annual report to a dataset that survives EU scrutiny.

- Anchor on your SECP IFRS S2 inventory. If you report in Phase 2 from 1 July 2026, you are already building a GHG Protocol Scope 1 and 2 baseline. Make that the single source of truth rather than starting a separate exercise for the EU.

- Push measurement down to the facility and process. Move from company-wide averages to mill-level and process-level data across spinning, weaving, dyeing, and finishing. Product attribution later depends on this granularity existing now.

- Attribute emissions to the product. Allocate facility emissions to product lines and, where synthetic content applies, to material inputs, so you can produce a per-product figure the moment CBAM or the DPP asks for one.

- Build supplier and material traceability. The DPP needs origin, composition, and production history. Start collecting verified data from yarn and fabric suppliers now, in a structured and repeatable format, not as a one-off audit before a shipment.

- Put it on an auditable system. Spreadsheets rarely survive a year-two assurance review, let alone product-level EU verification. Use a system that validates data and holds the audit trail from facility to product.

Spectreco's Compliance, Reporting and Disclosures advisory runs this exact sequence with Pakistani exporters, pairing the gap analysis with an AI-validated data layer on its cloud-native ESG platform so the numbers hold at facility and product level.

Frequently Asked Questions (FAQs)

The Bottom Line

The carbon-data reckoning for Pakistan's textile sector is not one deadline. It is CBAM edging toward polymers by 2030, the Digital Product Passport landing from February 2027, and a SECP mandate that already has textile firms reporting. The exporters that treat these as one dataset, built once and reused, will keep EU market access cheap. The ones that wait will rebuild the same numbers three times, under three separate deadlines.

Spectreco helps Pakistani textile exporters turn a SECP IFRS S2 inventory into CBAM and DPP-ready carbon data. Book an export carbon-data readiness assessment: we map your exposure, run the gap analysis, and stand up an auditable Scope 1 and 2 baseline on our ESG platform and Virtual Sustainability Office, with our Climate and Green Finance advisory team on the regulatory detail. Start with Spectreco's Pakistan ESG intelligence.

More From Our Blog

Your ESG Journey?