How to Collect Scope 1 and 2 Emissions Data for AASB S2

How to Collect Scope 1 and Scope 2 Emissions Data for AASB S2: An Australian Compliance Guide

Most Group 2 companies preparing for their first AASB S2 sustainability report focus on the disclosure. The harder work is what comes before it: building a defensible, repeatable, audit-ready emissions data process from operational sources.

Scope 1 and Scope 2 emissions are mandatory from your first reporting period under AASB S2. They are also the only disclosures subject to limited assurance from Year 1, conducted by the same auditor who signs off on your financial statements.

That is the key point most companies miss. This is not a sustainability estimate. It is an audited figure. Every litre of diesel, every kilowatt-hour of electricity, every refrigerant leak must trace back to a source document that your auditor can verify.

AASB S2 (Australian Sustainability Reporting Standard S2: Climate-related Disclosures) requires disclosure of absolute gross greenhouse gas (GHG) emissions separately in metric tonnes of CO2-equivalent for Scope 1 and Scope 2. Scope 3 is exempt in Year 1 for Group 2 companies but becomes mandatory from Year 2 — which means the data systems built now need to extend, not rebuild, when that obligation arrives.

This guide covers what Scope 1 and Scope 2 mean in the Australian context, how NGER reporting relates to AASB S2, what auditors will look for, and the six-step collection process that makes a sustainability report assurance-ready.

What Scope 1 and Scope 2 Mean Under AASB S2

Before collecting any data, the boundary question must be settled. AASB S2 requires companies to define which legal entities, facilities, and operating sites fall inside the reporting boundary — and to apply that boundary consistently with the financial reporting perimeter.

Sources: Clean Energy Regulator, NGER Measurement Determination 2008; AASB S2 paragraph 29(a)(v); Carbonly.ai, Scope 1 vs 2 vs 3 Australian context, April 2026.

The Boundary Decisions That Create Audit Risk

Two boundary questions catch companies repeatedly:

- Contractor equipment on your site. Whether a contractor's diesel excavator or generator counts as your Scope 1 depends on the operational control test. If you direct their health, safety, and environmental policies, the Clean Energy Regulator may treat those as your Scope 1 emissions under NGER. If they operate independently under their own policies, it is your Scope 3. The answer must be documented, not assumed.

- On-site solar generation. Electricity generated by rooftop solar and consumed on-site is not Scope 2 and not any scope. It does not appear in the GHG inventory. The moment electricity crosses a meter from the grid, it becomes Scope 2. Self-generated renewable energy consumed on-site is simply excluded.

Both decisions need to be recorded in a boundary-setting policy before data collection begins. Auditors will ask for it.

Does NGER Reporting Satisfy AASB S2 Scope 1 and 2 Requirements?

The short answer: no, not on its own. NGER reporting is facility-level and threshold-based. AASB S2 requires corporate-level boundary reporting using the GHG Protocol as the primary accounting standard. The two frameworks have meaningful gaps that must be closed before an AASB S2 disclosure is complete.

What NGER Covers

The National Greenhouse and Energy Reporting (NGER) scheme applies to facilities above 25,000 tonnes CO2e per year or corporate groups above 50,000 tonnes CO2e. It captures Scope 1 and Scope 2 from qualifying facilities. Scope 3 is not reportable under NGER at all.

Where the Gaps Are

- Below-threshold facilities. A network of smaller offices, depots, or retail sites, each below the NGER facility threshold, may be omitting material emissions from NGER submissions that must appear in the AASB S2 report. AASB S2 requires all emissions within the reporting boundary, regardless of size.

- Methodology priority. Updated AASB S2 standards now prioritise the GHG Protocol unless otherwise required by law. For companies with NGER-reporting facilities, the December 2025 amendments provide relief: NGER methodology can continue for those specific facilities, while the GHG Protocol applies to the rest of the group. This split approach requires a documented reconciliation for auditors.

- Reporting boundaries differ. NGER is organised around registered facilities. AASB S2 follows the financial reporting perimeter, the same entities consolidated in the financial statements. Companies must map the difference and document their approach.

The practical takeaway: use NGER as your operational data backbone for qualifying facilities, apply the GHG Protocol for the rest of the group, and document clearly where each methodology applies and why.

Sources: Greenbase, NGER vs GHG Protocol and the AASB S2 Shift, June 2025; Anthesis Group, ASRS and AASB S2 guide, January 2026; BDO Australia, Make Your Mandatory Sustainability Report Assurance-Ready, March 2026.

Choosing Your NGER Calculation Method

For Scope 1 sources where NGER applies, companies must select a measurement method for each emission source. NGER provides four methods, ranging from simple to precise.

Source: Clean Energy Regulator, NGER Measurement Determination 2008; CER Guidance on NGER reporting methods.

Two rules govern method selection:

- Consistency across years. Once a method is chosen for a source, companies must continue using it for at least four consecutive reporting years. Switching to a higher method is permitted. Switching to a lower method generally requires CER approval.

- Different methods for different sources are allowed. Method 1 can apply to vehicle fuel while Method 3 applies to a gas-fired boiler. What matters is that each source has a documented method choice with a clear rationale.

For most Group 2 companies starting from scratch in 2026, Method 1 is the practical starting point for most sources. It uses default emission factors from the Clean Energy Regulator and is well understood by auditors. The goal for Year 1 is a defensible baseline, not methodological perfection.

What Auditors Will Actually Check

Limited assurance on Scope 1 and Scope 2 emissions begins in Year 1 under ASSA 5000, the Australian Standard on Sustainability Assurance Engagements. Your financial auditor will apply the same evidential standards they use for financial statement line items.

The General Ledger Reconciliation

Every fuel and energy figure in the emissions inventory must reconcile to the general ledger. Diesel purchased in the accounts must match diesel consumed in the emissions calculation. Electricity billed must match electricity metered.

Unexplained differences between the financial accounts and the emissions data generate audit queries. These are slow and expensive to resolve at year-end. Resolve them during the year.

The Documentation Auditors Expect

Four things every auditor will ask for:

- A documented boundary-setting policy explaining which entities and facilities are included and why

- A Basis of Preparation showing how AASB S2, NGER (where applicable), and the GHG Protocol are applied — and where they interact

- Reconciled activity data tied directly back to invoices, meter reads, and the general ledger

- Emission factor records: which factor was used for each source, the source document (CER NGA Factors, supplier data, or direct monitoring), and the date the factor applied

Spreadsheets Will Not Survive Assurance

Spreadsheet-based carbon tracking does not produce the audit trail limited assurance requires. There is no version control, no change log, no access records, and no systematic link between source documents and calculated figures.

If your current process is a spreadsheet, treat building a purpose-built system as a Year 1 priority — not a Year 2 upgrade. The assurance engagement will expose the gap, and rebuilding mid-audit is a costly problem.

Sources: BDO Australia, Make Your Mandatory Sustainability Report Assurance-Ready, March 2026; eco-shaper, AASB S2 Group 2: Are You in Scope for 2026?, March 2026; AUASB, ASSA 5000, January 2025.

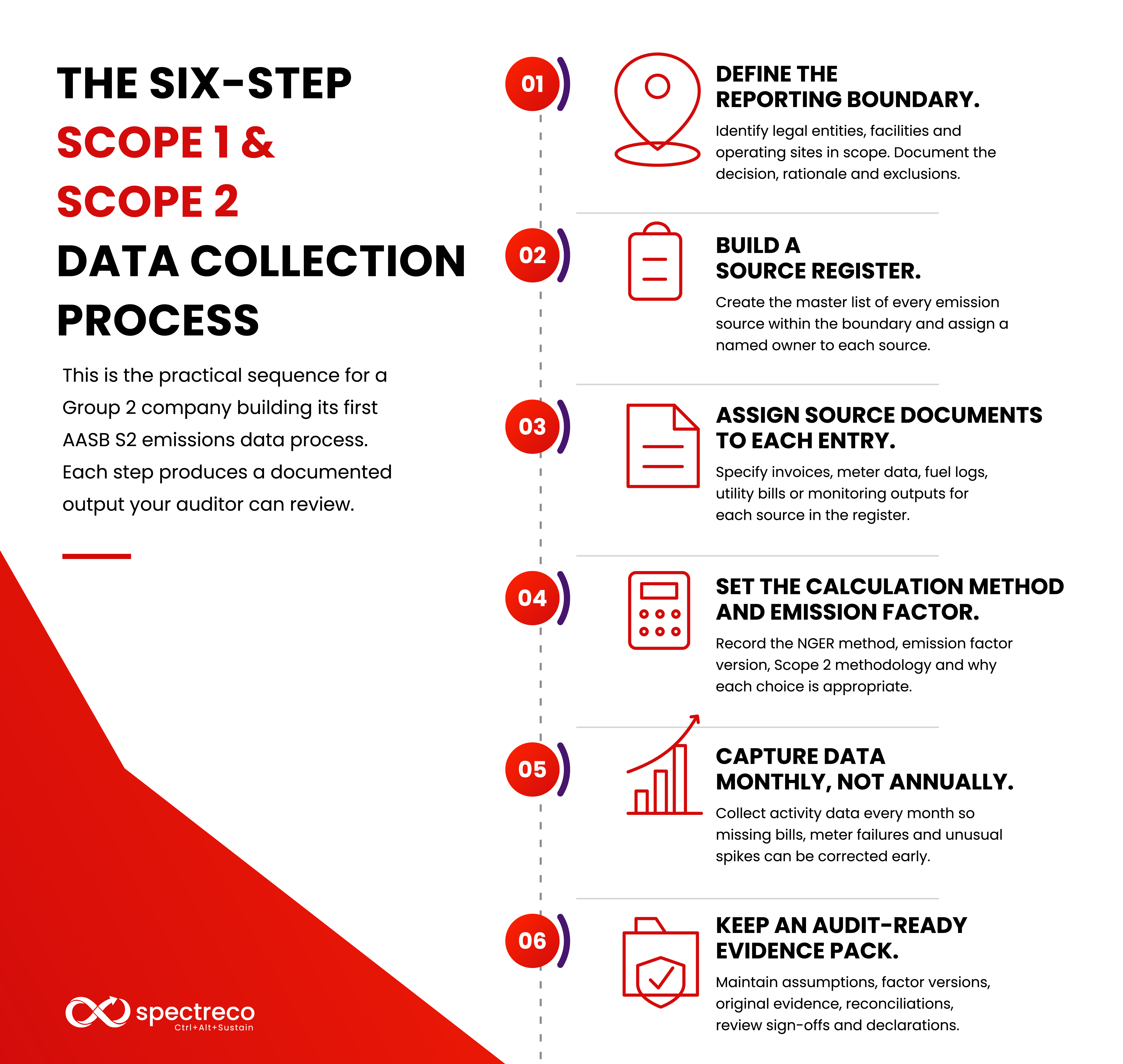

The Six-Step Scope 1 and Scope 2 Data Collection Process

This is the practical sequence for a Group 2 company building its first AASB S2 emissions data process. Each step produces a documented output your auditor can review.

- Define the reporting boundary. Identify which legal entities, facilities, and operating sites fall within the sustainability reporting boundary. Apply the same consolidation approach (operational control or financial control) used in the financial statements. Document the decision, the rationale, and any exclusions.

- Build a source register. Create a register of every emission source within the boundary: stationary fuel combustion, mobile fuel use, industrial processes, fugitive emissions (particularly refrigerants), and purchased electricity accounts. Assign a named owner to each source. This register is the master list your auditor will test for completeness.

- Assign source documents to each entry. For each source in the register, specify the primary evidence: supplier invoices, calibrated meter data, fuel delivery logs, utility bills, laboratory analysis, or continuous monitoring system outputs. The evidence type determines which NGER measurement criterion applies and what the auditor will request.

- Set the calculation method and emission factor. Record the NGER method (1 through 4) for each Scope 1 source, and the emission factor version used. For Scope 2, record whether location-based or market-based methodology applies and which NGA Factor version was used. Document why each choice is appropriate.

- Capture data monthly, not annually. Collect activity data every month. Anomalies, missing bills, meter failures, or unusual consumption spikes are far easier to investigate and correct while records are still accessible. Companies that collect annually discover problems after the financial year closes, when source data is harder to retrieve and auditors are already engaged.

- Keep an audit-ready evidence pack. Maintain a structured file containing: all assumptions and their basis, emission factor versions with effective dates, original invoices and meter exports, methodology notes, reconciliations to the general ledger, review sign-offs, and management declarations. This is the file your auditor opens first.

One process design point: data governance must be built for annual repetition, not a one-off project. Lock down owners, evidence requirements, review checkpoints, and change-control rules before the first reporting period begins. Consistency of method across years is a NGER requirement and an AASB S2 audit expectation.

Read the full AASB S2 compliance guide for Australian companies.

Frequently Asked Questions (FAQs)

AASB S2 compliance starts with operational data discipline. The sustainability report is the output. The emissions data process is what makes it auditable.

For Group 2 companies with a July 2026 start date, there are three months to confirm the reporting boundary, build the source register, set up monthly data capture, and reconcile activity data to the general ledger. That is achievable — but only if the process design happens now.

The companies that treat this as a documentation project, assembling last year's invoices into a spreadsheet in June 2027, will face audit queries, potential restatements, and a Year 2 Scope 3 obligation with no data foundation underneath it.

Spectreco works with Group 2 and Group 3 Australian companies to design AASB S2 emissions data collection processes, align NGER and GHG Protocol methodologies, and build audit-ready reporting workflows before the first sustainability report is due. Book a 30-minute AASB S2 data readiness assessment with our team.

Spectreco's Virtual Sustainability Office for Group 2 companies without internal ESG capability

Spectreco's ESG Reporting and Disclosures advisory for AASB S2 compliance support

Book an AASB S2 Data Readiness Assessment → spectreco.com

.jpg)

.jpg)

More From Our Blog

Your ESG Journey?