Green Sukuk & ESG Disclosure in the GCC: What Issuers Must Know

Green Sukuk and Sustainability-Linked Finance in the GCC: What Issuers Need to Disclose

The GCC sustainable bond market is not an emerging story. It is an executing one. S&P Global projects total sustainable bond and sukuk issuance across MENA to reach $20-25 billion in 2026. Saudi Arabia and the UAE together accounted for 68 percent of regional ESG sukuk volume through the first nine months of 2025 (Oren / Green Finance research, 2025). Global ESG sukuk outstanding crossed $50 billion by year-end 2025, a 23 percent year-on-year increase, according to Fitch Ratings.

For issuers in that market, the question has shifted. It is no longer whether to issue green sukuk. It is whether the disclosure infrastructure exists to support a credible issuance. This article covers what GCC issuers must disclose, which frameworks govern that disclosure, and where the gaps between Shariah compliance and ESG reporting still need to be closed.

What Is a Green Sukuk?

A green sukuk is a Shariah-compliant investment certificate whose proceeds are restricted to environmentally beneficial projects. It combines two distinct governance layers: Islamic finance principles (asset-backing, prohibition of interest, Shariah board approval) and green bond standards (use-of-proceeds restrictions, impact reporting, external review). This dual structure is set out in the ICMA, Islamic Development Bank, and LSEG Guidance on Green, Social and Sustainability Sukuk (April 2024).

The instrument satisfies both sets of obligations in a single issuance structure. A corporate or sovereign issuer in Riyadh or Abu Dhabi that wants to raise capital for a solar facility, a water treatment plant, or a green building portfolio can do so while remaining accessible to both Islamic investors and the growing pool of ESG-conscious conventional investors who would not otherwise participate in sukuk markets.

Sustainable sukuk expands that scope further, combining environmental and social use-of-proceeds categories, funding affordable housing or healthcare infrastructure alongside climate-related projects. The global sukuk market crossed $1 trillion outstanding at year-end 2025, with record issuance exceeding $300 billion during 2025 alone, up 25 percent year on year (Economy Middle East / Fitch Ratings, January 2026).

The Disclosure Framework: What Standards Apply?

Green sukuk disclosure sits at the intersection of three frameworks. Issuers operating in the GCC must understand all three.

ICMA Green Bond Principles and Sustainable Sukuk Guidance

The International Capital Market Association (ICMA) published its Guidance on Green, Social and Sustainability Sukuk in April 2024, developed in collaboration with the Islamic Development Bank and the London Stock Exchange Group. This guidance aligns sukuk labelling with ICMA's Green Bond Principles and Social Bond Principles.

Under this framework, issuers must disclose across four pillars:

- Use of proceeds: a clear list of eligible project categories with specific environmental objectives

- Process for project evaluation and selection: how projects are assessed against environmental criteria, including any exclusions

- Management of proceeds: how funds are tracked, ring-fenced, and allocated until deployment

- Reporting: annual impact reports covering both allocation of proceeds and quantified environmental outcomes

One known gap in the April 2024 guidance: it does not require ESG screening of the underlying Shariah assets used to structure the sukuk, only of the use-of-proceeds projects. This is a structural difference from conventional green bonds and remains an area of active discussion among Shariah scholars and sustainable finance practitioners. The RFI Foundation flagged this in its May 2024 review of the ICMA guidance as a risk that could be mitigated with clearer asset-level disclosure.

AAOIFI Governance and Accounting Standards

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) governs accounting and governance standards for Islamic finance instruments across GCC markets. AAOIFI's Governance Standard GS-12 (Sukuk Governance) and Financial Accounting Standard FAS-34 (Financial Reporting for Sukuk-holders) set the baseline for transparency between issuers and certificate holders.

AAOIFI's Shariah Standard No. 62, currently under review following 2025 public hearings, proposes stronger requirements on asset transfer and dissolution. If adopted as proposed, it would require clearer title transfer in asset-backed structures, with a compliance window of one to three years (Economy Middle East / Fitch Ratings, January 2026). GCC issuers planning new green sukuk should monitor this development, as the standard could affect structuring choices for issuances entering documentation in 2026 or 2027.

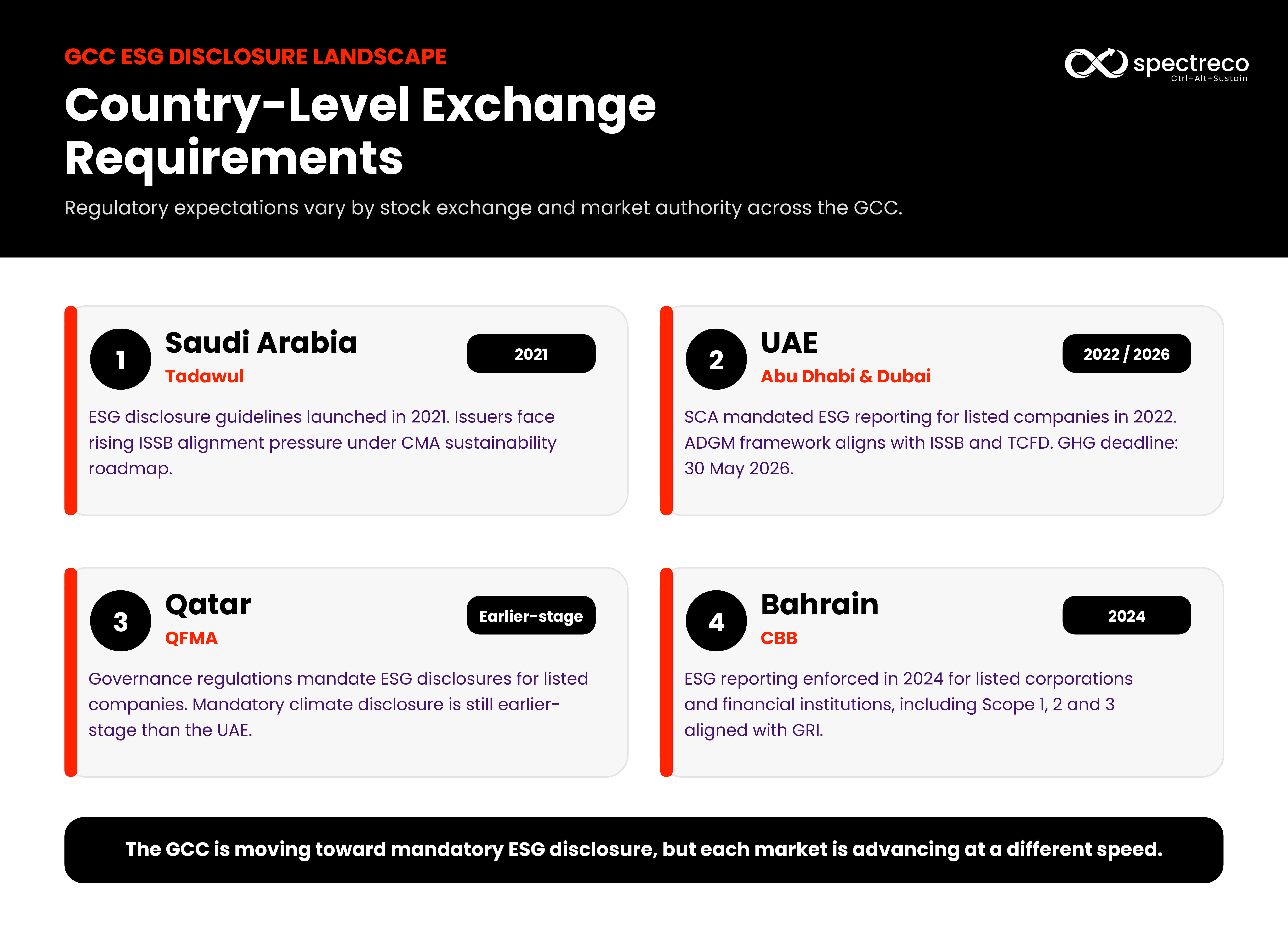

Country-Level Exchange Requirements

Regulatory requirements for ESG disclosure vary by stock exchange and market authority across the GCC:

- Saudi Arabia (Tadawul): The Saudi Exchange launched ESG disclosure guidelines in 2021 (Oren, ESG Reporting in the GCC, 2025). Listed issuers face growing pressure to align with ISSB standards under the Capital Market Authority's sustainability roadmap.

- UAE (Abu Dhabi and Dubai): The Securities and Commodities Authority mandated ESG reporting for listed companies in 2022. The Abu Dhabi Global Market introduced its Sustainable Finance Regulatory Framework in 2023, aligning with ISSB and TCFD (Oren, ESG Reporting in the GCC, 2025). The UAE 30 May 2026 GHG reporting deadline applies to entities registered under MOCCAE requirements.

- Qatar (QFMA): The Qatar Financial Markets Authority implements governance regulations that mandate ESG disclosures for listed companies (AIMS Press / Green Finance journal, January 2025). Qatar remains at an earlier stage of mandatory climate disclosure than the UAE.

- Bahrain: The Central Bank of Bahrain enforced ESG reporting requirements for listed corporations and financial institutions in 2024, covering Scope 1, 2, and 3 emissions aligned with GRI standards (Oren, ESG Reporting in the GCC, 2025).

What Do GCC Issuers Actually Disclose?

Disclosure for green sukuk in the GCC typically falls into three phases: pre-issuance, ongoing allocation, and annual impact reporting. Each phase carries distinct obligations.

Pre-Issuance: The Green Finance Framework

Before issuance, the standard market expectation is that the issuer publishes a Green Finance Framework. This document sets out:

- The eligible use-of-proceeds categories (renewable energy, clean transport, green buildings, water management, and so on)

- The governance process for project selection, including which internal committee or board function approves allocations

- The management and tracking mechanism for unallocated proceeds

- The commitment to second-party opinion (SPO) from an external ESG reviewer

- The Shariah supervisory board opinion confirming compliance with Islamic finance principles

In the GCC, the decentralized nature of fatwa issuance means Shariah board composition and methodology can vary across institutions. This creates divergent rulings on the same instrument structure. Malaysia's centralized model under the Securities Commission produces more consistent output. A 2025 World Bank-published study on Green Sukuk and the Environmental and Social Framework found that GCC jurisdictions show more divergent Shariah governance outcomes than Malaysia precisely because of this structural difference. GCC issuers working with international investors should document their Shariah governance clearly in the framework to avoid investor scrutiny during due diligence.

Post-Issuance: Allocation and Impact Reporting

Once proceeds are deployed, ICMA principles require annual reporting covering two dimensions:

- Allocation report: confirmation that proceeds have been applied to eligible projects, including a breakdown by category and the amount of unallocated funds

- Impact report: quantified environmental metrics for funded projects, such as GHG emissions avoided (tonnes of CO2 equivalent), installed renewable capacity (MW), water treated (cubic metres), or energy saved (MWh)

The quality gap in GCC impact reporting remains significant. Many issuers publish allocation reports that confirm proceeds have been spent but do not quantify environmental outcomes. Institutional investors, particularly European asset managers, increasingly require outcome data before making sukuk allocation decisions. The IFN UK Forum 2025 noted this expectation gap as a key friction point between GCC issuers and conventional ESG investors (Walkers Global, September 2025).

Where Shariah Principles and ESG Objectives Converge

The convergence is not forced. Maqasid al-Shariah, the objectives of Islamic law, include the preservation of life, progeny, intellect, wealth, and the natural environment. Environmental protection is embedded in the foundational ethics of Islamic finance, not bolted on to satisfy a Western capital market requirement. The ICMA, IsDB, and LSEG April 2024 guidance explicitly notes this alignment, stating that Islamic finance's contribution to sustainable development provides 'an additional layer of governance that helps direct issuance proceeds towards projects aligned with both Shariah standards and ESG criteria.'

This alignment produces structural advantages for green sukuk issuers. The dual governance layer of Shariah board review and ESG external review, while adding process complexity, reduces the risk of greenwashing claims. An instrument that has passed both a Shariah supervisory board and an independent ESG second-party opinion carries a stronger credibility argument than a conventional green bond subject to issuer self-certification.

For GCC issuers looking to attract both Islamic and conventional ESG investors, this dual oversight is a competitive positioning tool, not an additional compliance burden.

The Role of a Shariah-Compliant ESG Index

One of the structural gaps in green sukuk markets is the absence of a unified benchmark that measures both Shariah compliance and ESG performance in a single, investable score. Conventional ESG indices do not account for Shariah screening criteria. Shariah-compliant indices do not systematically incorporate climate and governance metrics.

Spectreco, an ESG technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore, signed a strategic agreement with the AlBaraka Forum for Islamic Economy at the 45th AlBaraka Islamic Economics Symposium in Madinah in April 2025 to develop the world's first Shariah-compliant ESG Index. The index is designed to provide asset managers, banks, and institutional investors with a unified benchmark that integrates Islamic finance principles with global ESG standards.

For issuers, a credible Shariah-ESG index changes the disclosure conversation. It gives institutional investors a standardized reference point for comparing issuers across markets, shifting the focus from framework compliance to actual ESG performance against a consistent methodology.

For GCC banks and asset managers building Shariah-compliant sustainable product suites, this kind of benchmark infrastructure is the missing layer between regulatory disclosure and investable decision-making. Learn more about Spectreco's climate and green finance advisory and how the platform supports ESG data management across GCC disclosure requirements.

How Should GCC Issuers Prepare?

Issuers at various stages of green sukuk readiness should focus on five areas:

- Establish or review your Green Finance Framework against the April 2024 ICMA guidance. If your framework predates this guidance, update the eligible use-of-proceeds categories and governance sections.

- Secure a credible second-party opinion provider with Islamic finance literacy. Not all SPO providers understand sukuk structuring. Misalignment between the SPO and the Shariah board opinion creates due diligence friction for investors.

- Build an impact data collection process before issuance, not after. Retrofitting emissions calculation or energy savings measurement post-issuance produces unreliable impact reports.

- Monitor AAOIFI Shariah Standard No. 62. If your current sukuk documentation relies on beneficial ownership structures that the new standard may restrict, begin scenario planning now.

- Map your country-specific exchange ESG disclosure obligations. A Saudi issuer on Tadawul has different mandatory disclosure requirements than a UAE issuer on the Abu Dhabi Securities Exchange, even for the same green sukuk structure.

Spectreco's AI-driven End to End ESG platform handles multi-jurisdictional ESG data management, including emissions tracking, impact reporting, and framework alignment across GCC and international disclosure standards. The Virtual Sustainability Office provides the ongoing program management to keep disclosure obligations current as requirements evolve.

.jpg)

.jpg)

More From Our Blog

Your ESG Journey?