AASB S2 for Australian Real Estate: What Property Companies Must Disclose

AASB S2 for Australian Real Estate: What Property Companies Must Disclose

Australian property companies are not waiting for a generic climate framework to tell them what matters. Climate risk already reprices assets, limits insurance access, and shifts where institutional capital flows. AASB S2 (Australian Sustainability Reporting Standard S2: Climate-related Disclosures), now mandatory under the Corporations Act 2001, translates that commercial reality into a legal disclosure obligation.

For ASX-listed real estate companies, REITs, and property trusts in Groups 1 or 2, this is not a distant planning exercise. Group 1 reporting began in January 2025. Group 2 obligations apply to financial years starting on or after 1 July 2026. For a full breakdown of thresholds and timelines, see:

What AASB S2 Means for Your Business Before July 2026

This article covers what AASB S2 requires specifically from real estate companies: the four disclosure pillars, sector-specific physical and transition risks, the tenant data problem, the role of GRESB, and what to prioritise before your first report lands with the Australian Securities and Investments Commission (ASIC).

Who in Australian Real Estate Must Report Under AASB S2

AASB S2 applies to entities that prepare annual financial reports under Chapter 2M of the Corporations Act 2001 and meet at least two of three size thresholds within a group.

For most major Australian REITs and listed property groups, Group 1 thresholds already apply. Group 2 catches a substantial cohort of mid-size property trusts, unlisted property funds that meet the Corporations Act reporting test, and diversified property companies. NGER Act reporters above the relevant emissions threshold are also captured regardless of size.

The group-level test is critical. An individually small property fund can be pulled into scope by the size of its parent or consolidated group. Fund managers should confirm in-scope status at group level before assuming any entity is exempt.

Why AASB S2 Is a Valuation Issue, Not Just a Compliance Issue

Before getting into the disclosure mechanics, the framing matters. AASB S2 uses a financial materiality lens: the standard applies to climate-related risks and opportunities that could reasonably be expected to affect cash flows, access to finance, or cost of capital over the short, medium, or long term.

For real estate, climate exposure is asset-level exposure. Physical risks affect occupancy rates, maintenance and insurance costs, capital expenditure requirements, and valuations. Transition risks affect building obsolescence, tenant expectations, and financing terms. A portfolio that cannot demonstrate climate resilience will face repricing by lenders, reduced tenant demand for non-green stock, and harder access to green finance facilities.

AASB S2 does not create these dynamics. It requires companies to report on them formally, under audit, and with directors personally liable for misleading statements.

Source: AASB S2 Climate-related Disclosures; Corporations Act 2001 (Cth); ASIC Regulatory Guide 280.

The Four Disclosure Pillars: What Real Estate Companies Must Address

AASB S2 is structured around four pillars derived from the Task Force on Climate-related Financial Disclosures (TCFD): Governance, Strategy, Risk Management, and Metrics and Targets. For property companies, each pillar carries sector-specific weight.

Governance

AASB S2 requires disclosure of how the board and management oversee climate-related risks and opportunities. This pillar is subject to limited assurance from Year 1, meaning your auditor scrutinises these disclosures in your first report.

ASIC Regulatory Guide 280 is explicit: directors must understand the climate-related risks and opportunities that materially affect the business and must ensure appropriate systems, internal controls, and oversight mechanisms are in place. The guidance references the McVeigh v REST case as a signal that directors may be personally exposed to liability for failing to consider foreseeable climate risks.

For property companies, governance disclosure means documenting which board committee holds responsibility for climate risk, how often climate is a standing agenda item, and whether climate performance is tied to executive remuneration. Sustainability teams can no longer hold this alone. Boards, audit committees, CFOs, asset managers, and facilities leaders all need defined responsibilities, because AASB S2 disclosures connect directly to capital planning, valuations, and investor communication.

Source: ASIC Regulatory Guide 280; Lexology/Materra, AASB S2 real estate sector analysis, May 2025.

Strategy

The strategy pillar requires disclosure of material climate-related risks and opportunities, their financial effects, and your Climate Transition Plan. For property companies, this means connecting asset-level climate exposure to business performance and decision-making, not treating climate as a separate sustainability narrative.

AASB S2 requires scenario analysis under at least two mandatory pathways:

- A 1.5°C scenario aligned with Australia's Climate Change Act 2022

- A high-warming scenario that well exceeds 2°C

For portfolios with assets across flood-prone coastal areas, cyclone corridors, or extreme-heat zones, the gap between these two scenarios can be material enough to affect asset valuations and impairment assessments. Portfolio managers need asset-level climate intelligence, not portfolio-wide averages, to produce credible scenario analysis.

Source: AASB S2 Climate-related Disclosures, September 2024; PwC Australia, Mandatory Sustainability Reporting guidance, 2025.

Risk Management

This pillar covers how the company identifies, assesses, and monitors climate-related risks, and how those processes integrate into the overall enterprise risk framework. AASB S2 uses the word 'integration' deliberately. Climate risk cannot sit in a separate sustainability register.

Real estate companies need documented processes showing climate hazard assessment feeding into acquisition due diligence, asset management decisions, and capital allocation. The standard is looking for evidence of genuine integration, not a parallel reporting exercise.

Metrics and Targets

From Year 1, companies must disclose:

- Scope 1 emissions: direct GHG emissions from sources owned or controlled by the entity, including building services, generators, gas use, and refrigerants

- Scope 2 emissions: indirect emissions from purchased electricity, heating, and cooling, including common-area energy

Scope 3 emissions become mandatory from Year 2. The AASB S2 December 2025 amendments introduced targeted relief for certain Scope 3 Category 15 financed emissions, effective for financial years beginning on or after 1 January 2027. Companies must also disclose any internal carbon price and climate-related capital expenditure where these are used in decision-making.

Source: AASB S2 Climate-related Disclosures; AASB S2 December 2025 amendments; ERM, ASRS 2026 Guide, February 2026.

For a practical guide to building Scope 1 and 2 data collection processes, see

How to Collect Scope 1 and 2 Emissions Data for AASB S2

Physical and Transition Risks Specific to Australian Property

Physical Risks

Physical risks in real estate are acute (event-driven) and chronic (long-term shifts). Australian property companies face material exposure across both:

- Flood: coastal and river-adjacent assets in Queensland, NSW, and Victoria face increasing frequency and severity

- Heat stress: assets in Western Australia and South Australia face rising cooling loads and reduced tenant habitability without capital investment

- Cyclone and storm surge: Northern Queensland and coastal Queensland assets

- Bushfire interface zones: peri-urban assets in Victoria, NSW, and South Australia

AASB S2 requires companies to assess what proportion of their portfolio is exposed to these hazards under both scenarios and to quantify financial effects where practicable. This is not a qualitative exercise for most portfolios. The standard expects location-specific hazard modelling, not a general statement that the portfolio faces climate risk.

Source: AASB S2 Climate-related Disclosures; OECD, Future-Proofing Real Estate Investment, December 2025.

Transition Risks

Transition risks hit Australian property through energy efficiency regulation, carbon pricing expectations, and investor repricing:

- Assets that cannot meet emerging minimum energy performance thresholds face reduced tenant demand and higher vacancy costs

- Older commercial stock without a credible retrofit pathway carries stranded asset risk

- Lenders are beginning to price carbon-misaligned collateral differently as green finance conditions tighten

- A high-carbon portfolio disclosed without a transition plan carries growing reputational exposure with institutional investors

Investors increasingly want to see how a portfolio will decarbonise through electrification, efficiency upgrades, renewable energy procurement, and capital works planning, not just a record of historical emissions. The transition plan is a disclosure requirement under the Strategy pillar, not an optional statement of intent.

Source: AASB S2 Climate-related Disclosures; S&P Global, Sustainable Bond Issuance data, 2025.

The Tenant-Landlord Data Problem

Real estate has one of the hardest data challenges under AASB S2. Most property companies do not control all the emissions data they need to report.

In multi-tenant commercial buildings, energy consumption and emissions data is often split across landlord-controlled base building systems and tenant-controlled tenancy loads. Utilities accounts sit with tenants. Sub-metering may not exist. Facilities managers hold data that does not feed into finance systems. Contractors and service providers hold maintenance records needed for emissions calculations.

This means the challenge for real estate is not only calculation methodology. It is obtaining complete, auditable source data across a portfolio that may span dozens of assets, hundreds of tenancies, and multiple service providers. Without a systematic approach to data collection, Scope 1 and 2 figures will be incomplete at the point of limited assurance review.

Property companies should treat data collection as an infrastructure build, not an annual year-end task. A portfolio-wide system for energy, emissions, asset risk, controls, and evidence retention is more efficient and more defensible than assembling disclosures asset by asset at reporting time.

Spectreco's ESG technology platform is built to consolidate operational emissions data across complex multi-site portfolios, with audit trail and methodology documentation built in.

Source: Lexology/Materra, AASB S2 real estate sector analysis, May 2025; ERM, ASRS 2026 Guide, February 2026.

Does Your GRESB Data Help With AASB S2?

Yes, significantly, but not completely. The GRESB (Global Real Estate Sustainability Benchmark) Real Estate Assessment forms the basis on which the IFRS S2 industry-based metrics for real estate have been modelled, per GRESB's July 2025 guidance. The ISSB explicitly references GRESB throughout its industry-based disclosure guidance, with definitions and calculations drawn directly from GRESB methodology.

For real estate companies already participating in GRESB, there is substantial overlap:

- GRESB GHG indicators cover Scope 1, 2, and 3 emissions across a portfolio, including both location-based and market-based figures

- GRESB's climate risk management indicators address transition and physical risk identification, scenario analysis, and resilience strategy

- GRESB target-setting sections align with AASB S2's targets disclosure requirements

GRESB participation does not automatically satisfy AASB S2. The standard requires a formal, explicit statement of compliance, limited assurance over Scope 1 and 2 disclosures from Year 1, and integration of climate risk into the financial reporting framework. GRESB is a voluntary benchmark. AASB S2 is a legal obligation with auditor sign-off and director liability attached.

If your GRESB data is current and well-documented, it gives your sustainability and finance teams a significant head start on the Metrics and Targets pillar. The gaps tend to appear in the governance documentation, financial effect quantification, and audit trail requirements that AASB S2 demands but GRESB does not require.

For a detailed mapping of where GRESB data satisfies AASB S2 requirements, and where it does not, see Does Your GRESB Score Count Towards AASB S2 Compliance?

Source: GRESB, The Interplay Between GRESB and IFRS S2 in Real Estate Sustainability, July 2025; GRESB Real Estate Assessment guidance, 2026.

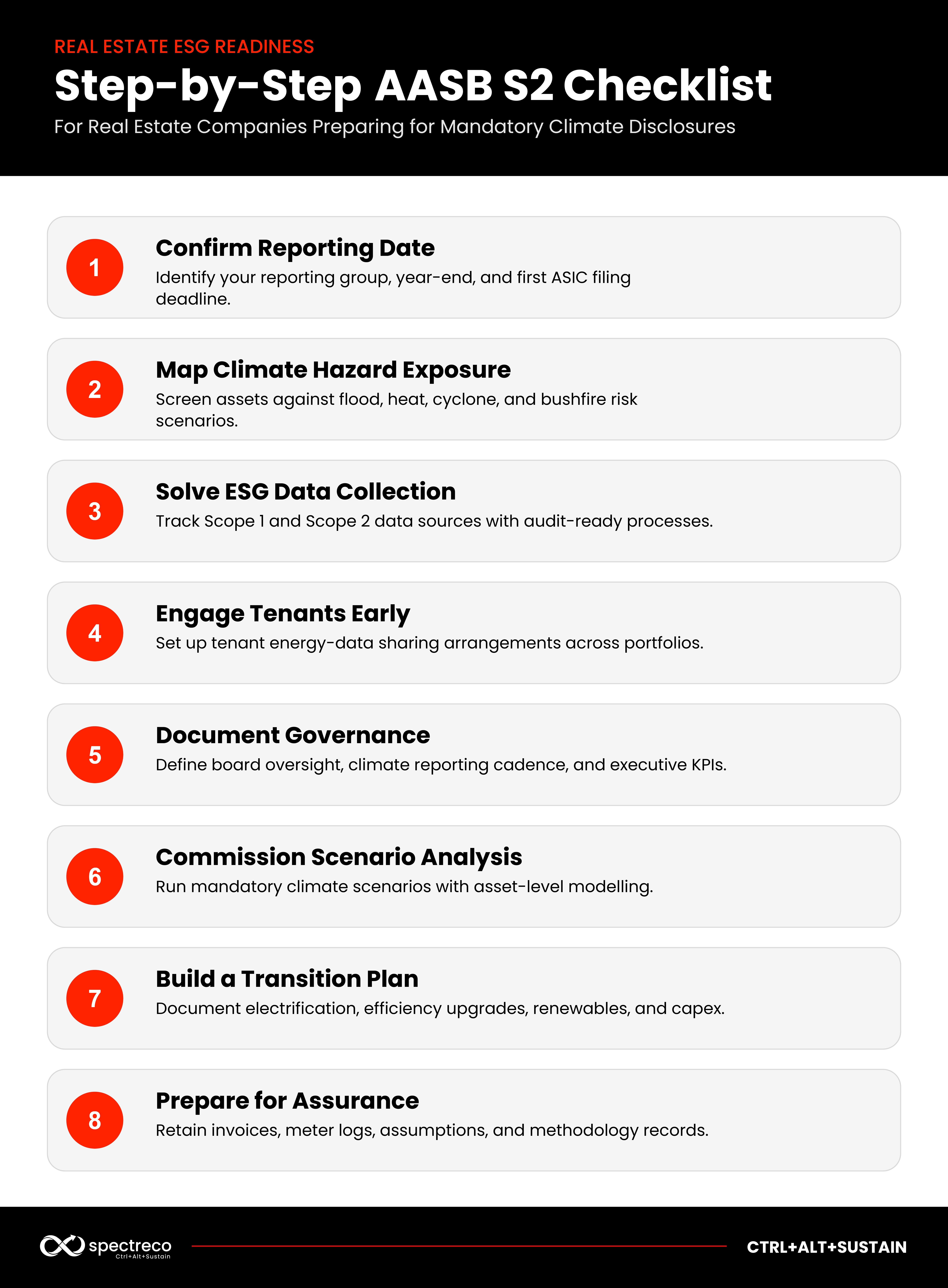

How to Prepare: A Step-by-Step Checklist for Real Estate Companies

- Confirm your group and first reporting date. A Group 2 company with a 30 June year-end reports for the year ending 30 June 2027, with the report due to ASIC by approximately October 2027. Companies with a December year-end have an earlier first reporting period. Confirm your exact date now.

- Map your portfolio for physical hazard exposure. Conduct an asset-level climate hazard screen under both the 1.5°C and high-warming scenarios. Identify which assets sit in flood, heat, cyclone, or bushfire zones and quantify exposure as a percentage of gross asset value.

- Solve the data collection problem before year-end. Identify every source of Scope 1 and Scope 2 data across your portfolio: base building meters, tenant sub-meters, gas accounts, generator fuel records, and refrigerant logs. Set up collection processes and audit trails now. Waiting until reporting season produces incomplete data and a difficult assurance conversation.

- Engage tenants on energy data access. In multi-tenant portfolios, start conversations with major tenants about data sharing arrangements. Lease provisions, Green Star obligations, and NABERS commitments are all leverage points. This takes time to negotiate and implement.

- Document your governance structure. Record which board committee oversees climate risk, the frequency of climate reporting to the board, and whether executive KPIs include climate metrics. These disclosures are subject to limited assurance from Year 1.

- Commission your scenario analysis. Two scenarios are mandatory. For most property portfolios, scenario analysis requires asset-level hazard modelling. It is the most resource-intensive requirement for companies without prior TCFD reporting. Start early.

- Begin your transition plan. The transition plan is not optional. Document how the portfolio will decarbonise across the investment horizon: electrification, efficiency upgrades, renewable procurement, and capital works. Connect it to your capital allocation process.

- Build assurance readiness from day one. Retain audit trails for meter data, invoices, engineering assumptions, methodology choices, and climate risk assessments. Assurance expectations are tightening each reporting cycle. Disclosures that cannot be traced to source data will fail review.

For specialist support on AASB S2 readiness, governance frameworks, and data infrastructure, see Spectreco's ESG Reporting and Disclosures advisory service.

Frequently Asked Questions (FAQs)

The Bottom Line

AASB S2 does not ask property companies to become climate scientists. It asks them to be honest, documented, and consistent about climate risk inside the same financial reporting framework they use for every other material risk. For property portfolios already managing physical climate exposure, stranded asset risk, and lender ESG requirements, much of that analytical work is already happening.

The difference now is that it is legally required, audited, publicly lodged, and attached to director liability. The companies that treat AASB S2 as a compliance exercise will produce compliant reports. The ones that treat it as a business lens will produce reports that protect asset values and attract capital.

Spectreco, an ESG technology and advisory firm with offices in Atlanta, Lahore, Lisbon, and Riyadh, works with property companies across Australia and the GCC to build AASB S2-ready data infrastructure, conduct portfolio-level climate risk assessments, and produce auditor-ready sustainability reports.

To understand where your portfolio sits against AASB S2 requirements, request a compliance assessment or explore our Net Zero and Decarbonisation advisory service.

.jpg)

.jpg)

More From Our Blog

.jpg)

Your ESG Journey?